Most people don’t fail at money because they’re lazy; they fail because nobody taught them how to line up cash flows with life goals. “Buy a home, pay for kids’ education, retire someday” sounds simple—until you try to put numbers and dates on it in 2025’s economy.

Below is a beginner‑friendly, problem‑oriented guide to financing major life goals, with real cases, hidden strategies, and a bit of history to show how we got here.

—

From pensions to DIY: why planning your goals got harder

If you were starting adult life in the 1970s, your playbook was different. A single stable job, a defined-benefit pension, cheaper housing relative to income, and far less student debt. Financial planning for life goals was almost “baked into” the system: work long enough, and a pension plus Social Security handled a big chunk of retirement.

Fast‑forward to 2025 and the landscape is almost inverted. Pensions are rare outside government and a handful of legacy employers. Retirement is mostly DIY via 401(k)s, IRAs, or their international equivalents. Housing costs in major cities outran wage growth for years. University tuition exploded. At the same time, we got better access to markets, cheaper investing, and digital tools—but more responsibility and risk.

So the core problem today isn’t lack of products; it’s lack of structure. Your income, debt, and goals are competing for the same dollars, and nobody is automatically optimizing them for you.

—

Step one: translate fuzzy dreams into price tags and dates

Most people start with vague wishes: “someday I’ll buy a house,” “I don’t want my kids drowning in loans,” “I’d like to retire early.” That vagueness is the enemy; you can’t finance a dream you never bothered to measure.

Let’s make this more concrete with a real‑life style case.

A couple in their early 30s in 2025: both work in tech, earn a combined $180k, rent a one‑bedroom, have $40k in student loans, and talk about (1) buying a home, (2) maybe an MBA for one of them, and (3) “stopping full‑time work” by their early 60s. When they visit one of the better financial planning services for life goals, the advisor doesn’t start with products. Instead, they ask three questions:

1. What do you want, in today’s dollars?

2. When do you want it?

3. How flexible are you on both?

Only after this do they bring in math. Suddenly “someday” becomes:

– Down payment in 5–7 years: $120k

– MBA in 4 years: $80k needed (after scholarships & savings)

– Retirement at 62: target $2.2M in today’s dollars

That translation from story to spreadsheet is the real beginning. Until you give each goal a timeline and a ballpark cost, any investing or budgeting is guesswork.

—

What history teaches about “safe” and “risky” choices

We tend to assume whatever feels normal now is permanent. But the last 50 years of economic history show how misleading that can be.

– In the 1980s, double‑digit interest rates made saving in cash surprisingly rewarding—but borrowing was painful.

– The 1990s–2000s saw strong stock market returns with bumps, then the dot‑com bust and 2008 crisis reminding everyone that “stocks only go up” is a myth.

– The 2010s and early 2020s brought near‑zero interest rates, cheap mortgages, massive run‑ups in asset prices, then inflation spikes after COVID and war‑related shocks.

– By 2025, many countries have higher but still moderate interest rates, stubborn inflation concerns, and expensive housing in many cities.

The point: what counted as “safe” for your parents’ financial goals (like leaving money in a savings account) may quietly be unsafe for you because inflation can eat it alive over 20–30 years. Historical context forces an uncomfortable truth: avoiding any investment risk is itself a big risk if you have long‑term goals.

—

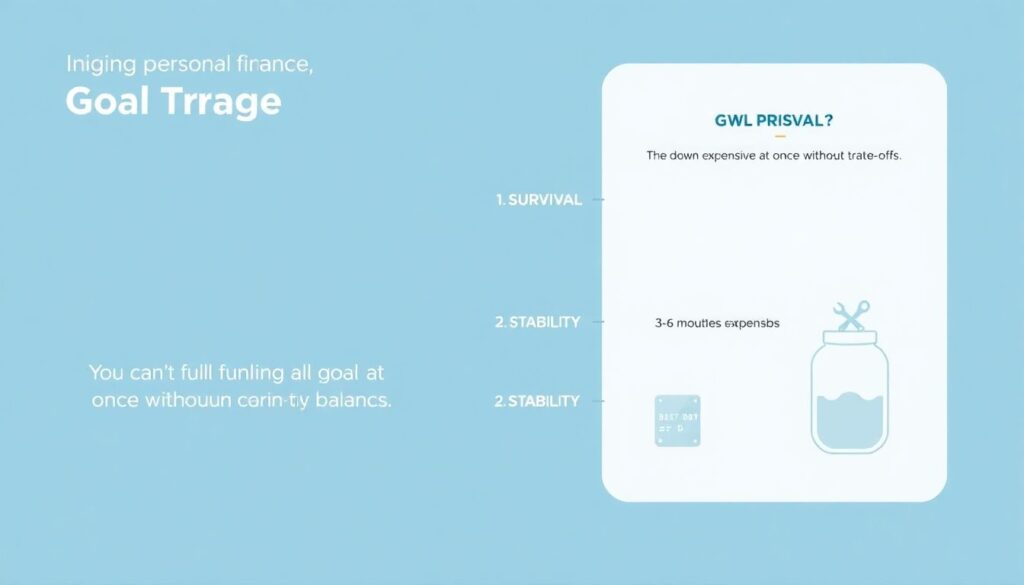

Ranking your goals: not everything can be priority #1

You can’t fully fund all goals at once without trade‑offs. Pretending you can is how stress and credit‑card balances spiral.

A minimal, beginner‑friendly way to triage goals is:

1. Survival – emergencies, basic insurance, minimum debt payments

2. Stability – pay down expensive debt, build 3–6 months of expenses

3. Growth – retirement investing, career upgrading

4. Lifestyle – housing upgrades, travel, kids’ education extras, early retirement

This hierarchy isn’t moral; it’s practical. Missing rent is more catastrophic than starting your children’s college fund a year late. Skipping health insurance to invest “more aggressively” might look smart on a spreadsheet—until one accident wipes out your accounts.

Hidden trick: when you feel overwhelmed, don’t ask, “How do I fund everything?” Ask, “What’s the most expensive mistake to make if things go wrong in the next five years?” Then bullet‑proof that area first.

—

Real cases: how different people financed the same goal

Take a fairly common target: paying for a child’s future education while still planning for retirement.

1) The “default” family

They saved sporadically, kept most extra cash in a basic savings account “so it’s safe,” and only ramped up contributions when their child turned 15. Inflation and low returns meant they arrived at college with far less than they expected, then leaned on high‑interest loans. Retirement contributions were paused to cover tuition.

2) The “structured” family

They started small when their child was a baby—just $100/month into a diversified education‑focused investment account—and nudged it up with every raise. They prioritized retirement first, then education, but used their longer time horizon to let compounding do most of the heavy lifting. By college time, they had a solid pot and needed only modest loans.

Both wanted the same thing; the difference was not discipline versus laziness but structure versus improvisation. This is precisely the sort of situation where the best financial advisors for retirement and education planning add value: they create a rule‑based system so that good decisions don’t depend on your willpower every month.

—

Non‑obvious solutions: when the “obvious” path is too expensive

Some life goals look impossible if you use the default script.

– Owning a home in an overheated market: rather than stretching for a 30‑year mortgage on a tiny apartment in a top‑tier city, some professionals in 2025 buy in less‑popular regions and rent the place out, while continuing to rent where they work. Over time, that first property becomes a stepping stone to later buying where they actually live.

– Funding education without drowning in debt: instead of front‑loading money into a single prestigious university, families are re‑engineering the path: community college or online courses for the first two years, then a transfer; co‑op programs where students alternate work and study; gap years to build savings and clarity before committing to expensive degrees.

Another underused angle is aligning goals with employer benefits. Many people ignore that some companies now offer student‑loan repayment support, restricted stock units, or even partial down‑payment assistance. Re‑negotiating your compensation package with these in mind can be more effective than trying to squeeze a little extra from bare‑bones budgeting.

—

Alternative ways to finance major goals (beyond “save and invest”)

Yes, saving and investing are core, but they’re not the only levers. Alternative methods can make big goals more realistic:

1. Income stacking

Side gigs aren’t new, but the mindset shift is: instead of “extra pocket money,” think of each secondary income as a dedicated funding stream for one specific goal. For example, freelance work dedicated 100% to an early‑retirement fund, while your main salary covers living costs and basic savings.

2. Geographic arbitrage

Historically, people moved for factory jobs or fertile land. In 2025, knowledge workers can often move for cheaper lifestyles. Earning a big‑city salary for a few years while living in a lower‑cost region (or fully remote in another country) can compress the time needed to hit a down payment or debt‑free milestone.

3. Shared ownership and co‑investment

Housing cooperatives, co‑living arrangements, or buying property with trusted friends or family can dramatically lower individual burdens—though they require robust legal agreements. In some countries, similar concepts exist for small business investment or farmland.

4. Education as a financial lever

Sometimes the best way to fund long‑term goals isn’t to shrink expenses but to increase earning potential by upgrading skills. Shorter, targeted programs (bootcamps, professional certifications) can yield faster payoffs than traditional degrees, especially if you negotiate partial sponsorship from employers.

These methods won’t fit everyone, but they illustrate a key idea: the path to funding big goals is often less linear than “cut coffee, buy index funds.”

—

How to choose a financial planner for long term goals

You don’t have to navigate all of this solo. But outsourcing your thinking to the first “expert” you meet is dangerous.

A few analytical filters help:

1. Compensation structure – Fee‑only planners (paid by you, not by product commissions) are less likely to steer you toward expensive investments that don’t serve your goals.

2. Goal‑orientation – Do they start with “How much can you invest?” or “What matters to you and when?” Strong planners talk about trade‑offs, uncertainty, and flexibility, not just market returns.

3. Scenario analysis – Ask how they model “what if” cases: job loss, illness, having kids earlier or later, or big market downturns.

4. Transparency and education – They should be willing to explain decisions in plain language until you could teach someone else the basics.

In practice, when people search something like goal based financial planning services near me, they’ll find a mix of traditional advisors, robo‑advisors, and hybrid services. A sensible beginner move is to treat the first meeting as an interview, not a commitment: you’re hiring a long‑term thinking partner, not buying a one‑time product.

—

What young professionals get wrong (and how to fix it)

If you’re early in your career, you actually have the strongest lever of all: time. Yet many young adults either procrastinate or chase quick wins.

The better alternative is building a simple system around personal financial planning packages for young professionals that typically include:

– A structured budget with automatic transfers to savings and investments

– A plan to crush high‑interest debt on a clear timeline

– Starter investment accounts (often with globally diversified index funds or ETFs)

– Insurance basics (health, disability, and, where needed, term life)

– Concrete saving targets for 1–2 medium‑term goals, like a relocation or further study

Surprisingly, the biggest win isn’t the specific product set; it’s the automation. Once contributions happen on payday, you reduce the mental friction of deciding every month whether to “be disciplined.”

—

Pro‑level tactics and lifehacks that beginners can still use

Professionals—planners, portfolio managers, CFOs—use a few habits you can borrow right away:

1. Reverse engineering

Start with the goal, discount for inflation, pick a reasonable return assumption, then calculate the monthly amount required. Adjust the goal if the required amount is absurd, instead of vaguely “saving what you can.”

2. Pre‑committing windfalls

Before bonuses, tax refunds, or vested stock hit your account, decide the percentage that goes to each goal. This avoids emotional spending and makes your progress “lumpy but fast.”

3. Separating “promise” money from “maybe” money

Pros don’t treat highly volatile investments as reliable funding for non‑negotiable goals. If you’re betting on a startup you work for, crypto, or concentrated stock positions, don’t let that be the only strategy supporting critical needs like retirement or housing.

4. Regular but infrequent reviews

Quarterly or semi‑annual check‑ins are enough for long‑term goals. Constant tinkering feels productive but usually just injects emotion.

By deliberately adopting these habits, even beginners can capture the most important benefits of professional discipline without needing a Wall Street background.

—

When it’s worth paying for advice instead of going DIY

There’s a persistent belief that all financial advice is either a scam or something you can replace with a few hours on YouTube. Sometimes that’s true; often it’s not.

Paying for expert guidance can be rational when:

– You have multiple competing goals (e.g., kids’ education, aging parents, business plans, and retirement)

– Your income is variable (founders, freelancers, sales roles)

– You’re dealing with tax complexity across countries or states

– You tend to either procrastinate or panic during market volatility

Modern firms offering financial planning services for life goals are gradually moving away from pure investment management toward holistic planning: cash‑flow design, goal mapping, risk management, and behavioral coaching. The investment portfolio is just how the plan gets implemented, not the plan itself.

—

Why “near me” matters less, and more, in 2025

Ten years ago, you almost had to choose local advisors and planners. By 2025, video calls, e‑signatures, and digital identity checks make geography less crucial. This is good because it widens your options beyond whoever has an office nearby.

At the same time, context still matters. When you look up something like the best financial advisors for retirement and education planning, you’d ideally want someone who:

– Understands your country’s tax rules, education systems, and retirement accounts

– Knows your local housing market realities

– Is familiar with your industry’s typical career paths and compensation structures

So while the phrase “near me” is increasingly about jurisdiction and context rather than physical distance, it’s still important that whoever helps you plan isn’t designing strategies in a vacuum.

—

Bringing it all together: a simple, analytical roadmap

To wrap this into something you can actually act on, here’s a stripped‑down sequence:

1. Name and date your top 3–5 goals

For each: what is it, when roughly, how much in today’s money, and how flexible?

2. Stabilize your present

Build a basic emergency buffer and ensure core insurance is in place so that one crisis doesn’t derail everything.

3. Run the math, even if rough

Use online calculators or a planner to backward‑calculate the monthly savings needed for each goal under reasonable return and inflation assumptions.

4. Prioritize and adjust

Expect some sticker shock. This is where you decide which goals can be scaled down, pushed back, or re‑engineered using alternative methods (moving, co‑ownership, different education paths).

5. Automate contributions

Set up automatic transfers aligned with your priorities. Treat them like non‑negotiable bills to your future self.

6. Review twice a year

Life will change; so will markets. Revisit assumptions, but don’t rebuild the entire plan every time the news turns gloomy.

7. Ask for help strategically

If you hit decision paralysis, explore a consultation with a planner. Even a one‑time planning session can clarify trade‑offs and give you a blueprint.

Financing major life goals in 2025 isn’t about chasing the latest hot investment or adopting an extreme minimalist lifestyle. It’s about matching your story with numbers, timeframes, and deliberate choices—drawing on history, using modern tools, and being honest about constraints. Once that structure is in place, you’re not hoping your future works out; you’re actively engineering it.