Kicking off your money journey can feel like staring at a blank map with no “you are here” sign. This guide walks you through budgeting and saving in a practical, step‑by‑step way, without pretending you’ll magically turn into a finance nerd overnight. The goal is simple: give you a clear system you can actually stick to, even if your income is irregular, modest, or you’ve “failed at budgeting” before.

—

Understanding Where Your Money Really Goes

Mapping Your Income With Brutal Honesty

Before asking *how to start a budget and save money*, you need to know what you’re working with. That means getting precise about income, not guessing. Pull out your last two to three months of pay stubs, bank statements, and any side hustle payments. If your income fluctuates, calculate your average monthly income, but also your *lowest* month in the last year. Use that lower number as your “safety baseline” so your plan doesn’t collapse the moment a month is weaker than usual. This more conservative approach is less exciting on paper, but it dramatically increases the odds that you can follow your budget without constant stress.

Tracking Spending Without Overcomplicating It

The second part of the picture is your spending. For at least 30 days, track every expense—even the tiny ones that feel irrelevant. You can use a simple notes app, a spreadsheet, or one of the best budgeting apps for beginners; the tool matters less than your consistency. At the end of the month, group expenses into broad categories: housing, utilities, food, transport, debt payments, fun, and “mystery money” (cash withdrawals or untracked card payments). That “mystery” part is often where a surprising amount of cash leaks out, so treat it as a signal, not a personal failure.

—

Essential Tools for a Simple, Real-World Budget

Digital and Analog Tools That Actually Help

Your toolkit should match your personality and lifestyle. Some people love apps, others stick to pen and paper. Aim for the simplest combination you are likely to use on a bad day when you’re tired, rushed, and not in the mood for money talk. At minimum, you need something to track spending, something to plan your month, and a way to separate money for different goals (like separate accounts or digital “buckets”).

Consider these types of tools:

– A banking app that shows real‑time balances and lets you create sub‑accounts or “pots” for goals.

– A basic spreadsheet (Google Sheets or Excel) with categories and totals you can copy month to month.

– A physical notebook or printed worksheet if writing things down helps you process better.

Using Apps Without Letting Them Run the Show

Many articles about personal finance tips for beginners talk about tools first, but tools are only as good as the rules you give them. When exploring the best budgeting apps for beginners, focus on apps that make it easy to: 1) connect your bank accounts, 2) categorize spending quickly from your phone, and 3) set clear targets for each category. Avoid apps stuffed with features you’ll never use; complexity often becomes an excuse to stop tracking. Think of the app as a calculator and reminder system, not a magic solution. You still decide what matters and where your money goes.

—

Building a Budget Planner for Monthly Savings

Designing Categories Around Your Real Life

Instead of copying someone else’s “perfect” template, build a budget that reflects your actual priorities and constraints. A budget planner for monthly savings should start with the non‑negotiables: rent or mortgage, utilities, transport, basic groceries, insurance, and minimum debt payments. Only then do you layer in savings and “wants.” This ordering is strategic: it makes sure fundamentals and progress (savings and debt reduction) are covered before lifestyle spending expands to fill every available dollar. If you discover your non‑negotiables already eat the entire paycheck, that’s not a reason to give up; it’s a clear signal that something structural needs attention—roommates, cheaper phone plan, different commute, or extra income.

A Simple Step‑by‑Step Budget Setup

Here’s one straightforward sequence you can walk through in an hour:

1. Write down your *take‑home* income for the month (after taxes and deductions).

2. List all fixed bills with due dates and amounts.

3. Estimate variable categories (food, fuel, personal spending) using your last month’s data.

4. Decide how much you can realistically send to savings and debt beyond the minimums.

5. Assign *every* dollar a job: bills, goals, or fun—nothing left “unplanned.”

This “zero‑based” style doesn’t mean you spend everything; it means unassigned money is deliberately labeled “savings” or “buffer.” That clarity is what keeps your plan from evaporating halfway through the month, because you’ve already decided in advance what “extra” money is for instead of letting it drift away in impulse buys.

—

Step-by-Step: Turning the Plan Into Daily Action

Weekly Check‑Ins Instead of One Big Monthly Panic

A common mistake is treating the budget like a once‑a‑month ritual—set it, then ignore it. Money is dynamic; transactions keep happening whether you look or not. A more workable approach is a 10–15 minute weekly review. Once a week, open your banking app or spreadsheet, and:

– Update your current category totals (food, fun, etc.).

– Pay any bills due in the next 7–10 days.

– Decide in advance what you’ll do with any leftover cash in categories that ran under.

These mini check‑ins turn budgeting from a huge emotional event into routine maintenance. Over time, they also improve your sense of how much you can safely spend on a night out or a weekend trip without blowing up the month. It moves you from guessing to informed decision‑making.

Automating the Boring Parts

Whenever possible, automate. Have your paycheck split so that a portion lands directly in savings or a separate “bills” account. Set up automatic transfers right after payday for your main goals: an emergency fund, debt reduction, and any short‑term targets like travel. Automation works because it removes willpower from the equation; you don’t wait to see what’s “left over” to save. Instead, saving becomes the first transaction, and regular spending adapts to what remains. This is especially useful if you struggle with impulse spending or feel tempted every time your balance looks “high” for a moment.

—

Saving in Real Life, Even on a Low Income

Strategies for When Money Already Feels Tight

When you’re wondering how to save money on a low income, a lot of standard advice feels disconnected from reality. You can’t “cut Starbucks” if you rarely buy it. The analytical question becomes: where is the *flex* in your budget, even if it’s small? Start by ranking your spending categories from most to least essential. Then examine the bottom of that list with curiosity, not blame. Can streaming services be rotated monthly instead of kept year‑round? Can you share subscriptions with family or roommates? Are there cheaper but acceptable alternatives for recurring costs like gym memberships, phone plans, or branded groceries? Aim for a series of small, sustainable cuts instead of one dramatic, miserable change.

Micro‑Savings and Incremental Wins

When your margins are thin, traditional targets like “save 20% of your income” may not be feasible. Instead, focus on creating *any* positive gap between income and expenses, even if it’s $10–$50 per month at first. Treat this not as a sign of failure, but as proof the system is working. Over time you can raise the number through a mix of smarter spending and small income boosts—occasional overtime, selling unused items, or a side project. What matters most is the habit of automatically moving that surplus into a separate account before you see it as “spendable.” This slow, steady approach is often the only realistic way forward in tight conditions, and it still compounds over years.

—

Practical Personal Finance Tips for Beginners

Making Saving Feel Less Abstract

Many people don’t save because their goals are fuzzy. “Be better with money” is too vague to motivate real behavior change. Instead, pick one to three concrete targets with numbers and deadlines: “Build a $600 starter emergency fund in six months,” or “Pay off the smallest credit card in eight months,” or “Save $400 for holiday travel by November.” Tie each goal to a dedicated sub‑account named after it. Every time money moves into that account, you see the progress, not just a bigger generic balance. This simple psychological shift turns saving from a chore into a visible scorecard of your choices.

Using Short Rules to Simplify Daily Decisions

Complex rules are hard to follow in real life, so reduce your system to a handful of quick guidelines you can remember under pressure. For example:

– “Any unexpected money (refunds, bonuses, gifts) is 50% to goals, 50% to fun.”

– “Large purchases over $100 get a 24‑hour cooling‑off period.”

– “If I go over in one category, I must lower another category to match it.”

These mini rules protect the budget without requiring constant calculations. They also reduce guilt: instead of feeling bad about every purchase, you simply ask, “Does this follow my own rule?” If it does, you can move on. If not, you either skip it or consciously break the rule knowing the trade‑off, which is still better than mindless spending.

—

Troubleshooting Common Budgeting Problems

When You Keep Blowing the Same Category

If you notice you constantly overspend in one area—say, dining out—that’s useful data, not a moral verdict. First, check whether your estimate was simply unrealistic. If you repeatedly budget $80 for something that reliably costs you $150, the number is wrong, not you. Raise that category closer to reality and reduce a lower‑priority area to keep the totals balanced. Second, look for patterns: certain days of the week, particular friends, or emotional triggers. Once you identify when and why the overspending happens, you can design friction: pre‑decide how many meals out you’ll have, withdraw cash for that purpose, or use a separate card just for that category so you see the limit approaching in real time.

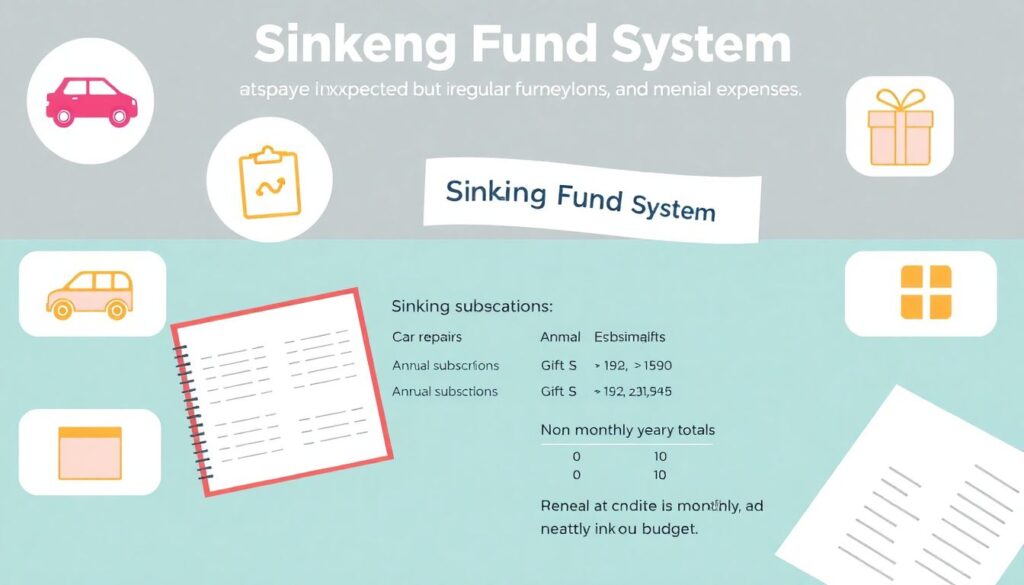

When Irregular Expenses Keep Blowing Up the Plan

Unexpected expenses are rarely truly unexpected; they’re usually just irregular—car repairs, annual subscriptions, gifts, medical co‑pays. To handle this, create a “sinking fund” system: you list non‑monthly costs, estimate their yearly total, and divide by 12. That monthly amount becomes a line in your budget, transferred to a dedicated savings bucket. For example, if car maintenance averages $600 a year, set aside $50 each month. Then, when something breaks, you’re not scrambling; you’re just using money already assigned to that purpose. Over 6–12 months, this dramatically lowers the chaos and makes your budgeting numbers much more stable.

—

Adjusting and Evolving Your System Over Time

Reviewing and Recalibrating Without Starting From Scratch

Your first budget is a prototype, not a permanent rulebook. Plan a short review every one to three months to check what worked, what didn’t, and what changed in your life. Did your rent go up? Did you get a raise? Did your priorities shift from debt payoff to building a larger emergency fund? You don’t need to reinvent the entire structure each time; you simply adjust numbers, add or remove categories, and refine your rules. Think of it like version updates to a piece of software—you iterate rather than reboot. This mindset keeps you from abandoning the system the moment life stops matching your original assumptions.

Pulling Everything Together

Budgeting and saving are not about perfection or deprivation; they’re about making your money behave a little more like a tool and less like an unpredictable storm. You start by seeing your current reality clearly, pick simple tools you’ll actually use, set up a budget planner for monthly savings that matches your life, and then keep tweaking as you go. With time, the combination of small structural changes, clear goals, and regular check‑ins transforms budgeting from something you dread into just another part of how you run your day‑to‑day life. The earlier you start, the more options you create for your future self—without needing to become a financial expert overnight.