Understanding What a Budget Really Is

Let’s kick things off with a simple definition: a budget is a plan for your money. It’s not a restriction—think of it more like a map that shows where your money is going rather than wondering where it went.

In technical terms, a personal budget is a financial tool used to allocate income toward expenses, savings, and debt repayment. It helps you track cash flow, avoid overspending, and make informed financial decisions.

Imagine your income is a pie. A budget slices that pie into categories: rent, groceries, savings, fun, and so on. You decide how big each slice is, depending on your goals.

Why Budgeting Matters More Than You Think

Many people associate budgeting with cutting back, but in reality, it’s about gaining control. Without a budget, you’re essentially driving blindfolded—you might get somewhere, but probably not where you want to be.

A well-crafted budget helps:

1. Prevent impulse spending

2. Reduce financial stress

3. Build savings intentionally

4. Achieve long-term goals like buying a house or retiring early

Consider this: budgeting is to finance what GPS is to navigation. You can technically get to your destination without it, but it’s a lot easier with a guide.

Types of Budgeting Methods

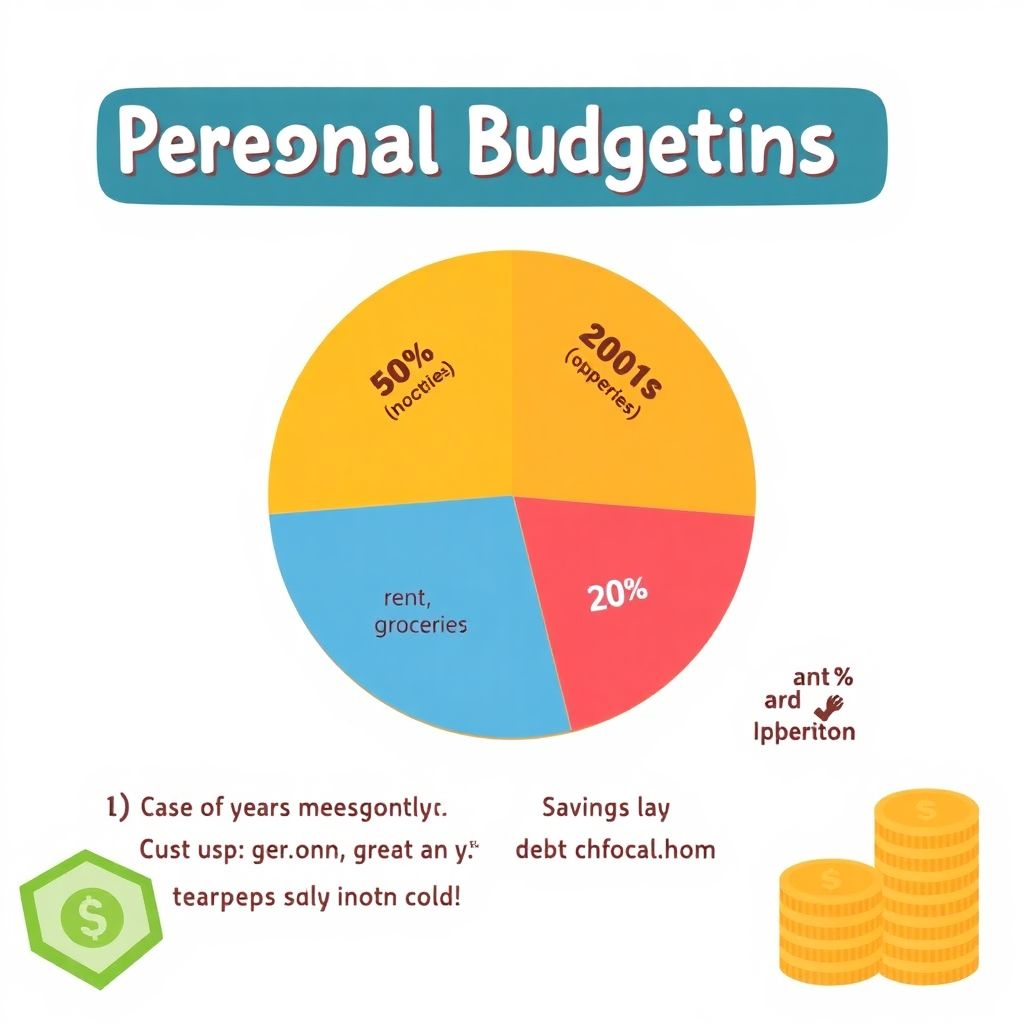

1. The 50/30/20 Rule

This is one of the simplest budgeting frameworks, especially for beginners. Here’s how it breaks down:

– 50% of your income goes to needs (rent, groceries, utilities)

– 30% to wants (dining out, entertainment)

– 20% to savings and debt repayment

Visual Diagram (Text Description): Picture a pie chart divided into three slices: half of it is your “needs,” roughly one-third is “wants,” and the last, smaller wedge is “savings & debt.” Easy to visualize, easy to follow.

This method is ideal for those who want a hands-off approach without tracking every penny.

2. Zero-Based Budgeting

With zero-based budgeting, every dollar gets a job. You assign every cent of your income to a category—until you’re left with zero unassigned dollars.

It’s more hands-on but incredibly effective for people who want to be meticulous and intentional with their money.

Comparison: Think of the 50/30/20 method as a flexible diet, while zero-based budgeting is like meal prepping every calorie—both work, but they suit different personalities.

3. Envelope System

This is the old-school, cash-in-hand method. You divide your money into envelopes labeled “Rent,” “Groceries,” “Fun,” etc. When an envelope is empty, that’s it—no more spending in that category.

This method is extremely helpful for people who struggle with self-control and want a tangible way to manage money.

How to Create Your First Budget

Creating a budget doesn’t have to be complicated. Here’s a step-by-step guide to get you started:

1. Calculate Your Net Income

This is the money you take home after taxes and deductions. Don’t use your gross income—it’ll give you a false sense of purchasing power.

2. List All Monthly Expenses

Include both fixed expenses (rent, subscriptions) and variable ones (groceries, entertainment). Look at past bank statements to spot trends.

3. Categorize and Prioritize

Divide expenses into “needs,” “wants,” and “financial goals.” Be honest about your spending habits—if you eat out five times a week, don’t budget for two and expect magic.

4. Allocate Funds Accordingly

Use a budgeting method (like 50/30/20) to assign portions of your income to each category.

5. Track and Adjust Monthly

Budgets are living documents. If something isn’t working, tweak it. Flexibility is key to long-term success.

Common Budgeting Mistakes to Avoid

Even with the best intentions, budgeting can go sideways. Watch out for these common pitfalls:

– Being too rigid: Life happens. Leave room for unexpected expenses.

– Ignoring irregular expenses: Think annual car registration or holiday gifts.

– Underestimating “wants”: You’re not a robot. Budget for fun or you’ll rebel.

– Not reviewing your budget: If you set it and forget it, you’ll lose track of progress.

Real-World Example: Anna’s Budgeting Journey

Anna is a 26-year-old graphic designer earning $3,500 per month after taxes. She used to live paycheck to paycheck, unsure where her money went.

She decided to try the 50/30/20 rule:

– $1,750 to needs (rent, bills, groceries)

– $1,050 to wants (subscriptions, clothes, dining out)

– $700 to savings and debt

After three months of tracking, she noticed she was overspending on restaurants. She adjusted her budget, cut dining out by $200, and increased her savings. Today, she has a $3,000 emergency fund and is paying off her student loans ahead of schedule.

Tools That Can Help You Budget Smarter

You don’t have to do it all manually. Here are a few tools to make budgeting easier:

– YNAB (You Need A Budget): Great for zero-based budgeting fans.

– Mint: A free app that tracks spending and categorizes automatically.

– Spreadsheets (Google Sheets, Excel): Ideal for customization if you like full control.

Final Thoughts: Budgeting as a Lifestyle, Not a Chore

Budgeting isn’t a one-time event—it’s a habit. The goal isn’t to restrict joy but to align your spending with your values. Whether you want to travel more, buy a home, or simply stop stressing about money, a realistic budget is your first step.

Start small, stay consistent, and adjust as you learn. The financial freedom you gain is well worth the effort.