Why budgeting on an irregular income feels so hard (and why you can totally handle it)

If your income jumps up and down every month, it can feel like your money has a mind of its own. One month you’re flush, the next you’re wondering how rent is already due again. Budgeting with irregular income isn’t about predicting the future perfectly. It’s about building a system that still works when life refuses to be consistent.

In 2025 more people than ever are living this way: freelancers, creators, Uber drivers, consultants, small business owners, remote contractors in multiple currencies. You’re not an exception anymore — you’re the new normal. The good news: people have been dealing with unpredictable income for centuries. We’re just putting modern tools and clearer thinking on top of an old problem.

—

From farmers and sailors to freelancers and coders: короткий исторический контекст

Irregular income is not a “gig economy” invention. Historically, many groups lived with wild swings in cash flow:

– Farmers earned most of their income after harvest.

– Sailors and traders got paid per voyage.

– Craftspeople and artisans depended on seasonal demand.

– Performers, writers, and artists lived from commission to commission.

Back then, the “budget” was brutally simple: store enough grain, salt meat, and save coins from a good season to survive a bad one. No spreadsheets, just survival. People intuitively learned how to save money on variable income because famine was a real possibility.

Fast-forward to the 20th century: the industrial era normalized stable salaries and monthly paychecks. Budgeting advice was built for factory workers and office employees with regular pay. Envelopes, then checkbook balancing, then early personal finance software — all assumed predictable numbers.

Then came the 2000s and 2010s: the rise of freelancing platforms, remote work, and side hustles. By the early 2020s, millions realized that the standard “50/30/20” salary-based budget didn’t work for them. Now, in 2025, financial planning for self employed with irregular income is a mainstream topic, not a niche footnote in a finance book.

You’re basically dealing with the same problem as a 17th-century merchant — but with better Wi‑Fi.

—

Three main approaches to budgeting on a fluctuating income

1. The “baseline + buffer” method (most beginner-friendly)

This method starts with one key question: “What’s the minimum I need each month to stay okay?” Not to live your dream life — just to keep the lights on and food in the fridge.

1. Calculate your bare-bones baseline:

– Rent/mortgage

– Utilities

– Groceries

– Transport

– Minimum debt payments

– Essential subscriptions (the ones you’d really struggle without)

2. Look at your income over the last 6–12 months.

Figure out:

– Your average monthly income

– Your lowest income month

3. Your goal in good months:

– Cover this month’s baseline.

– Then stack extra into a buffer account until you have at least 1–3 months of that baseline saved.

On high-income months, you’re feeding the buffer. On low-income months, you pull from the buffer to keep your lifestyle steady. You’re smoothing out the chaos.

This is usually the easiest way to start how to manage money with fluctuating income because you don’t have to predict precise numbers — you just protect a minimum.

—

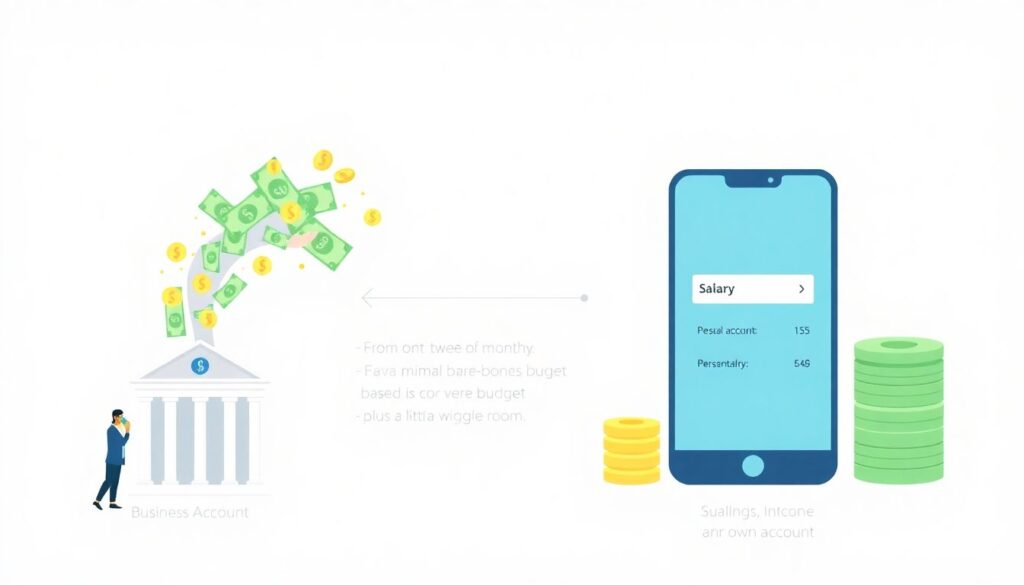

2. The “pay yourself a salary” method

Here you pretend you’re your own employer.

You send all incoming money to a business/income account. Once a month (or twice), you transfer yourself a fixed “salary” into your personal account — the amount is based on that bare-bones baseline plus some wiggle room.

Over time, the income account becomes your shock absorber.

If you have an amazing month, the extra stays in the income account instead of exploding your lifestyle. If you have a slow month, you still pay yourself the same “salary” as long as there’s enough built up.

This method is powerful if:

– Your irregular income is your main or only income.

– You want to avoid lifestyle whiplash.

– You want your personal money life to feel “normal” even when your business is turbulent.

It’s essentially turning unpredictable cash flow into something that *feels* like a regular paycheck.

—

3. The “percentage-based” method

Instead of fixed amounts, you work with percentages of each payment. For every dollar that comes in, you automatically divide it into buckets like:

– X% — essentials

– Y% — taxes

– Z% — savings and debt payoff

– W% — fun and non-essentials

This is inspired by systems like “profit first” and old-school envelope budgeting, updated for a digital era. It works especially well when your income swings widely but regularly (e.g., big project payments, commissions, seasonal work).

It’s great for psychological consistency: each time you get paid, you know money is getting split in a healthy way, even if the total changes.

—

Comparing the different approaches (and when each one shines)

Let’s line them up conceptually — without tables, just straight talk.

– Baseline + Buffer

– Best for: beginners, side hustlers, people just getting organized.

– Strength: simple; focuses on survival first.

– Weakness: if you don’t actively maintain the buffer, you slip back into chaos.

– Pay Yourself a Salary

– Best for: full-time freelancers, small business owners, contractors with deeply irregular months.

– Strength: your personal money feels stable; great for long-term planning.

– Weakness: needs discipline and a separate account; slower gratification in big months.

– Percentage-Based

– Best for: people comfortable with numbers, those with irregular but frequent payouts, commission-based earners.

– Strength: scales up and down automatically; avoids forgetting taxes or savings.

– Weakness: the math can feel annoying at first; very small payments can be fiddly.

You don’t have to marry just one. Many people mix them: for example, a percentage-based split flowing into a salary-style system, with a buffer as backup. That might sound complex, but in practice, apps and automation take most of the pain out.

—

Tech tools vs. low-tech methods: плюсы и минусы

In 2025 you’ve got more tools for budgeting with irregular income than any generation before you. But more tools doesn’t automatically mean more control.

Pros of using modern tech

– Automation

Rules in your banking app can instantly send, say, 25% of every incoming payment to a tax sub-account. No “I’ll do it later” trap.

– Real-time visibility

You can see in seconds how much is in “Bills,” “Buffer,” “Fun,” and “Taxes” instead of guessing.

– Historical data and analytics

Trends over 6–24 months help you see your real average income and worst-case months, which is gold for planning.

– Sync across currencies and platforms

Especially for digital nomads and remote workers getting paid from multiple countries.

The best budgeting apps for freelancers in 2025 typically emphasize multiple income streams, project-based tracking, and automatic category rules rather than just “monthly paycheck budgeting.”

—

Cons and pitfalls of relying on tech

Technology helps, but it doesn’t think *for* you.

– Over-complication

Too many categories, rules, and dashboards can paralyze you instead of helping you act.

– False sense of security

Logging into a polished app *feels* like progress even if you’re not actually sticking to any plan.

– Subscription creep

Paying for five financial tools “for organization” can eat a meaningful chunk of your irregular income.

– Data fatigue

A dozen charts won’t save you if you ignore the simple question: “Can I afford this *this month*?”

Low-tech methods — paper notebooks, basic spreadsheets, or an envelope system — still work in 2025. They’re slower but can force you to think more clearly about each decision. Some people actually budget better when they physically write numbers down.

—

How to choose the right approach for *you* (without overthinking)

You don’t need the perfect system; you need a system you’ll actually use when you’re tired and stressed.

Ask yourself:

– Do I hate math or love it?

– Do I prefer one big planning session or tiny decisions every time I get paid?

– Do I already use apps daily, or do I lose interest fast?

A few starter recommendations:

– If you’re overwhelmed and just starting

– Use the baseline + buffer method.

– Goal: know your minimum, build 1–2 months of that minimum as fast as you reasonably can.

– If freelancing is your full-time gig

– Combine pay yourself a salary with a small percentage-based system for taxes and savings.

– Treat your income like a business, even if you’re a one-person show.

– If you’re detail-oriented and like control

– Experiment with percentage-based budgeting per payment.

– Adjust percentages quarterly as you learn your real inflows and outflows.

Whichever you pick, commit to a 90-day experiment. The clarity comes from seeing your own patterns, not from hunting for a magic method online.

—

Step-by-step: a simple beginner’s budgeting workflow for irregular income

Let’s put it all together into something you can actually follow.

Step 1: Separate accounts (stop mixing everything)

At minimum, create:

– Income/Business account — all payments land here.

– Personal spending account — only your “salary” or transfers land here.

– Optional but highly recommended:

– Tax sub-account

– Emergency/buffer account

This physical separation does half the discipline work for you.

—

Step 2: Find your real baseline

Write out your true essentials for a normal month. Be honest.

– Housing

– Utilities

– Groceries and basic household items

– Transport

– Insurance

– Necessary digital tools (for work and life)

Total this. That’s your baseline. Add 10–20% on top for “small surprises” unless your life is extremely predictable (it probably isn’t).

—

Step 3: Study your last 6–12 months

Look back at all your income:

– Highest monthly income

– Lowest monthly income

– Average monthly income

If you’re brand new with no history, be conservative. Assume your actual income will be closer to your lower expectations than your hopes — at least for planning.

Use this info to decide:

– How big a buffer you need to feel safe.

– How much you can realistically pay yourself as a “salary” each month.

—

Step 4: Create simple rules for each payment

For every time you get paid, you might do something like:

– 25% → tax sub-account

– 10% → savings or debt repayment

– The rest → income/business account, from which you pay yourself your planned “salary” on a set date

This blends the percentage-based method with salary-style stability.

Over time, adjust those percentages. If tax season hurts, increase the tax cut. If your buffer feels too small, funnel more into it.

—

Step 5: Decide how you’ll say “no” during good months

The hardest part of how to save money on variable income isn’t during bad months — it’s during the good ones. That’s when lifestyle creep sneaks in.

Before your next big payout hits, decide:

– How much of a big payment is allowed to go to fun?

– What *must* go to:

– Taxes

– Buffer

– Long-term goals (education, house fund, gear upgrades)

When the money arrives, follow the script you wrote when you were calm, not your feelings in the moment.

—

Tech trends in 2025 that can actually help (not just look cool)

A few 2025 trends are particularly useful if your income fluctuates:

– Bank-integrated “bucket” systems

Many banks now let you create labeled pockets under one account — “Rent,” “Taxes,” “Buffer” — and auto-route percentages of each deposit. This makes percentage-based budgeting incredibly easy.

– AI-powered cash flow predictions

Some apps now scan your past gigs, invoices, seasonality, and even client behavior to give you a probabilistic forecast of your next few months. Not perfect, but much better than guessing.

– Invoice and budget integration

Freelance and creator tools increasingly link your invoices directly to your budget categories. Once a client pays, the app can immediately split the money according to your preset rules.

– Global-friendly tools

As more people earn in multiple currencies, apps increasingly handle auto-conversions, country-specific tax estimates, and multi-currency budgets — crucial for digital nomads and remote contractors.

The key is to pick one or two tools that fit your style rather than chasing every shiny new feature.

—

Mindset shifts that make irregular income less stressful

A big part of budgeting with irregular income is psychological. You’re dealing with uncertainty, and that can trigger anxiety — even if you’re earning decent money overall.

Helpful mindset shifts:

– Annual thinking, monthly action

Your *months* will be uneven. Aim for your *year* to be stable. Check: “Did I cover my total annual basics and save some?” rather than panicking about a single bad month.

– Buffers are non-negotiable business expenses

Don’t treat your buffer as “extra savings” you might raid for random wants. Treat it as rent for living with freedom and flexibility.

– Low-income months are data, not failure

When you hit a weak month, ask: “What can I learn? Was this seasonal? A one-off? A sign to market more?” Curiosity beats shame.

In other words: you’re not broken. The old salary-centric budgeting advice just wasn’t written for you.

—

Putting it all together

To wrap it up, here’s a simple, realistic roadmap for how to budget for irregular income as a beginner:

– Separate your accounts so you can *see* what’s what.

– Know your baseline; build a buffer that covers it for at least a month or two.

– Choose one core method — baseline+buffer, salary-style, or percentage-based — and commit to it for 90 days.

– Add tech where it clearly reduces friction, not just because it’s trendy.

– Review monthly, think annually, and adjust your system as your income stabilizes or grows.

You’re dealing with an old human problem using 2025 tools and knowledge. With a bit of structure, your fluctuating income can become a source of flexibility and opportunity instead of constant stress.