Most people don’t need a perfect budget. They need a simple system that survives real life: late paychecks, impulse buys, surprise bills and all. Let’s break down how to build a budget that actually sticks, especially if you’re just starting out and money already feels tight.

—

Why Most Beginner Budgets Fall Apart

When people talk about budgeting for beginners, they often suggest rigid spreadsheets or ultra-frugal challenges. On paper these look flawless; in practice they collapse within weeks. Основные причины:

1. The plan ignores irregular expenses (gifts, car repairs, annual subscriptions).

2. The system is too complicated to follow when you’re tired or stressed.

3. It doesn’t leave any room for fun, so you “rebel” against your own rules.

4. There’s no feedback loop: you don’t regularly compare plan vs. reality.

A budget that sticks is less about math and more about behavior. You need a structure that helps you make slightly better choices, month after month, instead of demanding perfection every single day.

—

Core Approaches to Budgeting: Comparison for Beginners

Zero-based budgeting vs. percentage-based budgeting

When you’re learning how to create a budget that works, you’ll quickly run into two big schools of thought: zero-based budgeting and percentage-based budgeting.

Zero-based budgeting means you give every dollar a specific job: bills, savings, debt, fun, everything. Income minus expenses equals zero (not because your account is empty, but because every cent is assigned on purpose).

Percentage-based budgeting uses rules of thumb like “50% needs, 30% wants, 20% savings/debt.” You don’t track every small transaction; you mostly watch the big buckets.

For many beginners, especially those who want a monthly budget planner for beginners, a hybrid ends up working best: use percentages to set rough targets, but assign specific amounts to your highest‑priority categories such as rent, utilities, groceries, debt and emergency savings. That way, you don’t drown in detail but also don’t lose control.

—

Case Study: Anna, the “Spreadsheet Perfectionist”

Anna, 27, tried budgeting with a color-coded spreadsheet that tracked 40 categories. She lasted three weeks. Each missed receipt felt like failure, so she stopped opening the file altogether.

We switched her to a zero-based approach with only 8 categories (rent, utilities, groceries, transport, debt, savings, fun, other). At the start of the month she assigned her income to these buckets. During the month she only checked three things:

1) Did rent and utilities get paid?

2) Is there money left in “groceries”?

3) Is she hitting her minimum savings target?

Her tracking became “good enough” instead of “perfect.” Six months later she still follows this pattern and has built a small emergency fund, which never happened with her old spreadsheet.

—

Different Styles of Budgeting: Envelope, Digital, and Automatic

The classic envelope system

The physical envelope system is one of the oldest tools for budgeting for beginners. You withdraw cash, split it into envelopes (food, gas, fun, etc.), and when the envelope is empty, that category is done for the month.

Pros:

– Very tangible. You can literally see when money is running out.

– Great for impulse spenders; it forces friction before each purchase.

Cons:

– Inconvenient in a world of online shopping and subscriptions.

– Harder to track recurring digital payments like streaming services or apps.

For people who struggle to “feel” digital money, a temporary envelope phase (2–3 months) can reset habits, then you can move back to cards and apps.

—

Digital category systems

Most modern tools imitate envelopes but in digital form. You create categories, assign amounts, and track spending against them. This is the core engine behind many of the best budgeting apps for beginners.

Pros:

– Handles both card payments and cash.

– Easier to analyze trends across months.

– Often syncs with bank accounts, reducing manual data entry.

Cons:

– Can encourage passive behavior: “the app will figure it out,” and you stop thinking consciously.

– Subscription costs, which matter if you’re focused on how to manage money on a low income.

The real question: do digital tools help you pay attention, or do they let you zone out? A good app makes your decisions more visible, not less.

—

Automation-first budgets

An automation-first budget leans heavily on scheduled transfers: paycheck comes in, then money automatically moves to savings, debt payments and bills. You only “see” what’s left for flexible spending.

Pros:

– Reduces decision fatigue.

– Less temptation to spend savings that never hit your visible balance.

Cons:

– If your income is irregular, fixed automation can lead to overdrafts.

– Easy to forget what’s happening and lose the sense of control.

For people with stable salaries, auto-transfers to savings and debt are powerful. For freelancers or gig workers, automation needs to be more flexible and often weekly instead of monthly.

—

Technology in Budgeting: Pros and Cons in 2025

Pros of modern budgeting tech

In 2025, the tech side of personal finance has evolved beyond simple expense trackers. Many apps now use bank APIs and basic machine learning to categorize spending, estimate upcoming bills, and even forecast cash flow.

Key advantages:

1. Speed and convenience. Transactions auto-import, so you’re not entering every coffee by hand.

2. Pattern recognition. Apps highlight trends, like “your average grocery bill rose 18% in the last 3 months.”

3. Goal tracking. You can set goals (emergency fund, vacation, debt payoff) and watch progress visually.

Downsides and hidden risks

The downsides are more behavioral than technical:

– Data overload. Charts, graphs, and dozens of category breakdowns can make you feel informed without driving real change.

– Security and privacy. Every extra financial app is another place where your data sits; you need to vet them.

– Subscription creep. Paying $10–15 a month for three different tools just to “stay organized” can quietly eat up savings.

The best budgeting apps for beginners are the ones you actually open at least once a week. Bells and whistles matter less than whether the app nudges you to adjust behavior when you slip off track.

—

Practical Case: Low-Income Budget That Still Allows Breathing Room

Case Study: Marcus, working with a tight income

Marcus, 32, works in retail with fluctuating hours. After rent and bills, his leftover money felt too small to bother with a budget. He assumed budgeting was for people with “extra” cash.

We approached his situation differently:

1. Calculated his average three‑month income, not his best or worst month.

2. Listed his guaranteed bills: rent, utilities, phone, minimum debt payments.

3. Created just three flexible categories: food, transport, “life happens.”

This is a textbook example of how to manage money on a low income: the budget’s main goal is survival stability, not aggressive saving. Once Marcus consistently covered basics, we added a tiny buffer: $10 per paycheck into a mini emergency fund. After a year, that fund handled two car repairs that otherwise would’ve become credit card debt.

The key insight: even a very small, simple budget creates more control than “I’ll just see what’s left.”

—

Step-by-Step: How to Build a Budget That Sticks

A simple 5-step roadmap

If you’re exploring budgeting for beginners and feel overwhelmed, focus on building a durable, low-friction system. Here’s a straightforward process:

1. Map your money in and out.

List all income sources (after tax) and your non-negotiable expenses: housing, utilities, groceries, transport, debt minimums. Use your last 2–3 months of statements, not guesses.

2. Create 3–5 flexible categories.

Don’t start with 20 categories. You might use: Essentials (food + household), Transport, Fun, Miscellaneous, Savings/Debt Extra. Your goal is clarity, not microscopic detail.

3. Assign limits before the month starts.

This is the heart of how to create a budget that works: you decide in advance what each dollar will roughly do. Adjust until income minus planned spending is at least zero (preferably with some savings).

4. Track weekly, not daily.

Pick one “money day” a week. Spend 15–20 minutes checking where you stand versus your targets and adjusting the rest of the month. Weekly check-ins keep you from drifting off course.

5. Iterate after each month.

Monthly review: Which categories were underestimated? Overestimated? Adjust amounts, not just your guilt levels. A budget that sticks is one you keep editing as your real life shows up.

—

Choosing Your Tools: Paper, Spreadsheets, or Apps?

Paper and notebooks

Paper-based budgets and handwritten logs are underrated, especially for people who need to reconnect with their money tangibly.

Benefits:

– Forces slow, deliberate thinking.

– Zero app learning curve.

– No digital distractions.

Drawbacks:

– Harder to analyze long-term trends.

– Easy to misplace or stop updating when you get busy.

Paper is a decent starting point for the first 1–2 months if you’ve been avoiding your finances. Once you’re more comfortable, many people switch to a digital monthly budget planner for beginners for easier tracking.

—

Spreadsheets

Spreadsheets sit between paper and apps. You control the structure and logic, which appeals to analytical minds.

Strengths:

– High flexibility; you can customize categories, formulas, and visuals.

– One-time setup can serve you for years with small tweaks.

– Free (or nearly free) using Google Sheets or similar tools.

Weaknesses:

– Manual data entry unless you use add-ons.

– Intimidating if you’re not comfortable with formulas.

If you like numbers and want to truly understand your cash flow, a well-designed sheet can be a powerful alternative to commercial apps.

—

Budgeting apps

By 2025, the landscape of budgeting apps has matured: many connect directly to your bank accounts, offer AI-based categorization, and have goal dashboards.

When evaluating the best budgeting apps for beginners, look for:

1. Simplicity of setup. If you feel lost in the first 15 minutes, it’s probably not your app.

2. Active reminders. Gentle nudges to review your budget or flag suspicious spending.

3. Offline resilience. Can you still use it meaningfully if sync breaks for a week?

Avoid chasing every new feature. You want a tool that supports your process, not a hobby that consumes your time while your actual finances remain messy.

—

Recommendations: How to Pick the Right Method for You

Match the system to your personality and lifestyle

Choosing a budgeting approach is like choosing a workout routine: the “best” one is the one you’ll keep doing. A few guiding questions:

1. How much detail do you tolerate?

– Hate details: percentage-based or super-simple category budget.

– Love details: zero-based budgets with well-defined categories.

2. How often does your income change?

– Stable salary: monthly automation works well.

– Irregular income: plan in two-week or weekly cycles; build a “buffer month” fund.

3. Do you spend more impulsively online or offline?

– Offline spender: consider a partial cash/envelope system for your biggest problem area (e.g., restaurants).

– Online spender: use app-based limits and keep your card details off shopping sites to add friction.

—

Case Study: Sofia, the “All-or-Nothing Starter”

Sofia, 24, repeatedly tried extreme money challenges: “No spend January,” “Only $50 a week,” and so on. She always saved a little in challenge weeks, then overspent heavily afterward, wiping out all progress.

We reframed her budget around sustainability, not heroics. She:

1. Identified one key leak (delivery food).

2. Put a realistic cap on that category instead of banning it.

3. Created a “guilt-free” fun budget, small but clearly defined.

The result: overall monthly spending dropped 12%, but without the binge–restrict cycle. Her success came less from discipline and more from designing a budget that fit her actual habits.

—

2025 Budgeting Trends Beginners Should Know

Trend 1: Cash-flow forecasting for everyday users

Budgeting tools in 2025 are increasingly focusing on future cash flow, not just past transactions. Instead of only saying, “You spent $300 on dining last month,” they’re beginning to say, “If you keep this pattern, your account may hit $50 by the 27th.”

For someone learning budgeting for beginners, this forward-looking view is crucial. It turns money management from post-mortem analysis into early-warning signals, giving you time to adjust before you overdraft.

—

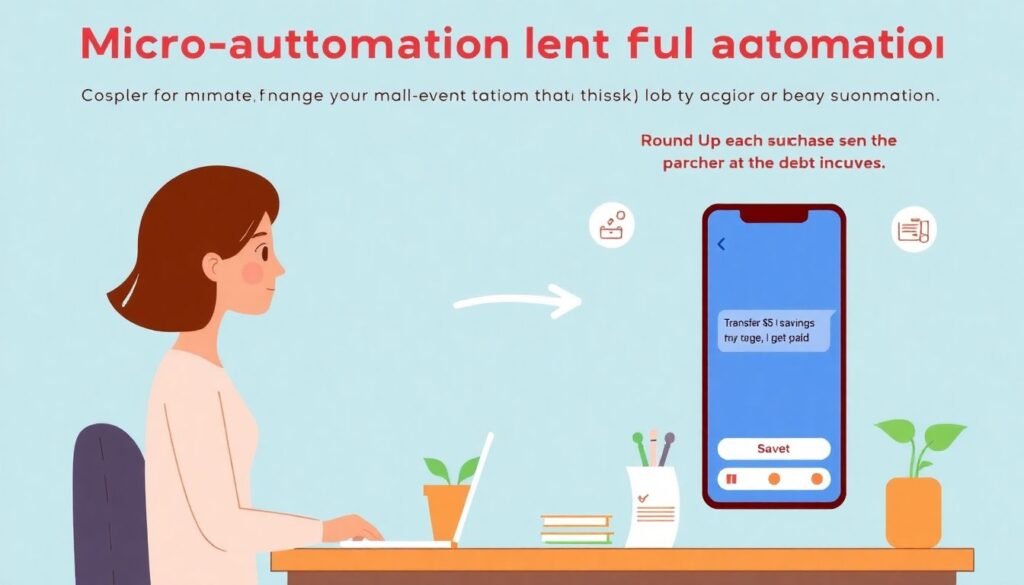

Trend 2: Micro-automation instead of full autopilot

Full automation can be risky if your financial life isn’t stable. Newer trends favor micro-automation: small, event-based rules like “transfer $5 to savings every time I get paid” or “round up each purchase and send the difference to debt.”

This approach supports how to manage money on a low income by allowing tiny, consistent wins without locking you into big, inflexible payments.

—

Trend 3: Values-based and mental health-aware budgeting

More people now design budgets not just around numbers, but around energy and mental health. They intentionally budget for rest, hobbies, and small luxuries that prevent burnout and rebound spending.

Apps and coaches increasingly emphasize questions like:

– “Which expenses genuinely make your life better?”

– “Where are you spending out of stress, boredom, or comparison?”

A budget that sticks in 2025 often includes a small “joy” or “sanity” category on purpose, even when money is tight, because it keeps the entire system psychologically sustainable.

—

Bringing It Together: Build a Budget That Survives Real Life

A durable budget is not a one-time document; it’s a living system you revise as your life shifts. Start with the simplest version that covers your core needs, then layer on details only when you consistently follow the basics.

If you remember only three things from this overview on how to build a budget that sticks for beginners, let them be these:

1. Choose a method that matches your personality, not someone else’s ideal.

2. Use technology as a helper, not a substitute for paying attention.

3. Review and adjust every month—small tweaks compound over time.

Real progress with money is rarely dramatic. It looks like slightly fewer financial surprises, gradually growing buffers, and a sense that you’re finally the one telling your money where to go, instead of wondering where it went.