Most people don’t start budgeting because they’re bad with money.

They start because life has a habit of throwing curveballs — layoffs, medical bills, broken cars, canceled contracts. A budget is your way of saying: “I can’t control everything, but I can be ready.”

Below is a conversational, no-nonsense walk-through of how to build a buffer for uncertain times, with real examples, expert recommendations, and practical tools you can start using today.

—

Why a Buffer Matters More Than a Perfect Plan

You don’t need a flawless spreadsheet to change your financial life. You need a small, consistent gap between what comes in and what goes out. That gap is your buffer — and it’s what keeps a bad week from turning into a bad year.

Think of it this way: every euro or dollar you don’t spend today is a tiny vote for your future freedom. One vote isn’t much. A few hundred votes in a row — that’s a safety net.

Behavioral finance expert Dr. Sarah Newcombe often says that people don’t stay calm in crises because they’re “disciplined”; they stay calm because they’re “prepared.” Budgeting isn’t punishment, it’s preparation.

—

How to Start a Budget for Beginners Without Overthinking It

If you’re wondering how to start a budget for beginners without getting stuck in 50-line categories and complicated rules, use this simple “3-bucket” method. It’s a step by step budgeting guide you can set up in one evening.

Long story short: you’ll track three things only.

1. What you must pay (needs)

2. What you choose to pay (wants)

3. What you pay your future self (savings and debt payoff)

Here’s a straightforward way to start:

– List your monthly income (after taxes).

– Subtract fixed needs: rent/mortgage, utilities, groceries, transport, basic insurance, minimum debt payments.

– Decide a starter amount for savings (even 2–5% is fine right now).

– Whatever is left is your “guilt-free” wants money — eating out, streaming, hobbies, gifts.

That’s it. You now have a basic budget. No fancy templates required.

Money coach Ramit Sethi puts it bluntly: “You don’t need a perfect plan, you need a plan you’ll actually follow.” Start simple enough that you can’t talk yourself out of it.

—

Inspiring Real-Life Examples: Tiny Steps, Big Buffers

Let’s look at how this works in real life — not in theory.

Example 1: The Freelancer Who Stopped Panicking Every Sunday Night

Marta, a graphic designer, used to dread the end of each month. Payments from clients were random, and any late invoice meant stress. She started by tracking her spending in a notes app for just two weeks.

She found two quiet money leaks: daily coffee + convenience food. She didn’t cut them completely; she just halved them, saving about $90 a month. She set a rule: every time a client paid her, 10% went straight to a “buffer account.”

One year later, she’d built a two-month emergency fund. When a big client suddenly paused work, it was still stressful — but not terrifying. She had time to respond, not just react.

Example 2: The Family That Went From Overdrafts to Options

A couple with two kids felt “too late” to start. They were always chasing next month’s paycheck. They created a minimal budget and chose one priority: no overdraft fees.

They sold unused stuff in their garage and raised $400. That cash went into a separate account they never touched for daily spending. It became a mini-buffer.

Over 18 months, they slowly increased automatic transfers to savings every time one of their expenses dropped (cheaper phone plan, paid-off car loan, etc.). Today, they have three months of expenses saved. The magic wasn’t a big salary. It was stacking small, boring wins.

—

How Much to Save in Emergency Fund: The Realistic Version

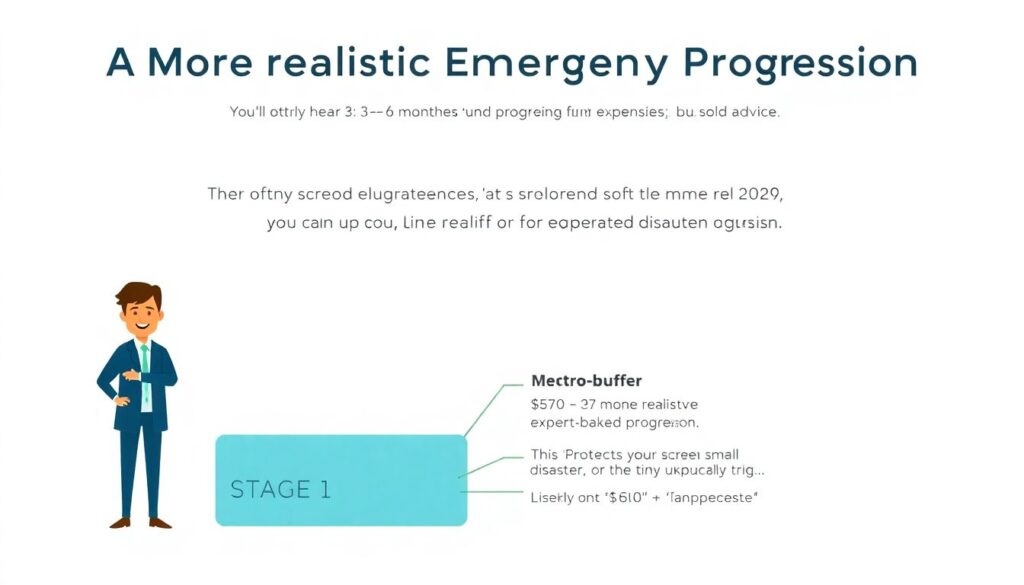

You’ll often hear the rule: 3–6 months of expenses. That’s solid advice — but if you’re starting from zero, it can sound like “climb Everest by Friday.”

Here’s a more realistic, expert-backed progression:

– Stage 1: Micro-buffer — $250–$500

This protects you from the tiny disasters that usually trigger credit card debt: a flat tire, a broken appliance, a medical visit.

– Stage 2: Starter emergency fund — 1 month of bare-bones expenses

Focus on what it takes to keep the lights on and food on the table. This is your “I can survive a short storm” money.

– Stage 3: Full emergency fund — 3–6 months of essentials

If your income is unstable (self-employed, freelance, commission-based), consider aiming for the higher end of that range.

When you’re asking yourself how much to save in emergency fund, don’t aim for perfection on day one. Aim for the next milestone. A fully funded buffer is built in layers, not in one heroic month.

Certified Financial Planner (CFP) Paula Pant recommends turning this into a number you can see:

“Write down your actual monthly essentials, multiply by three. That number is your North Star. You might reach it in 18 months or five years. What matters is that every month, you move closer.”

—

From Confusion to Clarity: A Step-by-Step Budgeting Guide

To make this actionable, follow this short step by step budgeting guide, then refine it week by week.

1. Find your real monthly baseline

– Pull the last 1–3 months of bank and card statements.

– Highlight essentials: rent/mortgage, groceries, transport, utilities, insurance, minimum loan payments.

– Add them up. That’s your survival number.

2. Set a monthly savings target (even tiny)

– Pick a starting percentage: 2–10% of income into savings.

– Automate this transfer to a separate savings account right after payday.

3. Create simple spending categories

– Needs (fixed + variable essentials)

– Wants (fun, dining out, shopping, subscriptions)

– Future (savings, investing, debt overpayments)

4. Choose your tracking method

– App, spreadsheet, or pen-and-paper. The best tool is the one you’ll use without hating it.

5. Check in once a week, not once a year

– Spend 10 minutes on “Money Monday” (or any day you like).

– Look at what you spent, what’s left, and what needs adjusting.

This is budgeting in real life: not punishment, not perfection, just regular, honest check-ins with your numbers.

—

Tools of the Trade: Best Budgeting Apps for Beginners

You don’t need apps, but they help a lot when life is hectic. Some of the best budgeting apps for beginners are built to be visual and forgiving, not rigid and stressful.

Here are common types of tools and how they can support you:

– Automatic trackers

These link to your bank accounts, categorize spending, and show trends over time. Great if you want “set-and-see” clarity and hate manual entry.

– Envelope-style apps

These let you “assign” money to categories (food, rent, fun, savings) as soon as it hits your account. Once a category is empty, it’s your signal to stop…or consciously move money from another envelope.

– Spreadsheet templates

Perfect if you like customization, want full control, and don’t mind entering numbers. Google Sheets and Excel have free starter templates.

Look for three things: simplicity, clear reports (not overwhelming dashboards), and reminders or alerts that you can adjust. If your tool stresses you out, it’s the wrong tool — not a sign you’re bad with money.

—

How to Build a Financial Safety Net That Matches Your Life

A safety net isn’t just a single emergency fund. It’s a set of layers that protect you from different kinds of uncertainty. That’s the heart of how to build a financial safety net that actually works.

Think in layers:

– Layer 1: Basic buffer

Your first $250–$500, then one month of bare-bones expenses.

– Layer 2: Full emergency fund

3–6 months of essentials, adjusted for your type of job and dependents.

– Layer 3: Risk protection

Adequate health insurance, basic life insurance (if people depend on your income), and disability coverage if available.

– Layer 4: Long-term resilience

Retirement contributions, upskilling, and diverse income streams.

Financial psychologist Dr. Brad Klontz notes that “resilience isn’t the absence of risk; it’s the presence of margin.” That margin is what your budget and buffer quietly create for you in the background.

—

Expert Recommendations: Habits That Actually Move the Needle

Money experts don’t all agree on everything, but they do tend to align on a few powerful habits for beginners.

They recommend that you:

– Automate what matters

Set up automatic transfers to savings and automatic bill payments when possible. Use your laziness in your favor — if you forget, money still moves to the right place.

– Decide your “enough” before spending

Before going into a store or opening a shopping app, decide your limit. If you planned to spend $40, and you see something for $80, that’s a conscious decision, not an “oops.”

– Name your savings accounts

“Emergency fund,” “Freedom fund,” “Moving abroad,” “Career break.” Names create emotional connection. You’re less likely to raid “Emergency Fund” than “General Savings.”

– Use pain-free increases

Every time you get a raise or pay off a bill, increase your savings rate before you adjust your lifestyle. You’ll barely feel it — but your buffer will.

Behavioral economist Shlomo Benartzi summed it up well with his “Save More Tomorrow” idea: commit now to saving more later. You don’t have to be a hero today; you just need a better default for tomorrow.

—

Cases of Successful “Budget Projects”: When Budgeting Changes More Than Money

Treat your budget like a personal project with a clear outcome: “Build a 3‑month buffer in two years.” That mindset shift alone can change how you feel about the process.

Case 1: The “Project Buffer” Challenge

A 29-year-old teacher decided to treat her finances as a 12‑month experiment. She gave it a name: “Project Buffer.” She:

– Picked a realistic target: $3,000 in an emergency fund.

– Set up a separate savings account labeled “Project Buffer.”

– Posted a monthly progress bar on her fridge.

She found one extra income source (tutoring twice a month) and made one cut (swapping two takeout nights for homemade pasta). The changes weren’t extreme — but she stuck to them because it felt like a project, not a punishment. She hit $3,000 in 11 months.

Case 2: The Team Budget at a Small Startup

A 7‑person startup was constantly on edge about cash flow. The founder introduced a simple team-level “budget buffer” rule: for every $10,000 of monthly revenue, $1,000 was automatically moved into a business emergency fund.

They treated this like a non-negotiable expense. Within a year, they had a three‑month runway saved. When one client delayed payment, they didn’t have to lay anyone off. The internal stress dropped dramatically — and with less panic, the team actually performed better.

Both cases show one thing: consistency beats intensity. A good budget is a long-term relationship, not a crash diet.

—

How to Grow Your Money Skills: Recommendations for Development

Once you’ve built a basic buffer, the next step is developing your financial skills so you’re not just stable, but progressing. Think of it as “leveling up” your money game.

Short, practical ways to grow:

– Learn one concept per week

Interest rates, inflation, index funds, basic taxes, debt snowball vs. avalanche. One idea at a time is enough — you don’t need a degree.

– Practice “mini experiments”

Try a no-spend weekend, a cash-only week for groceries, or a subscription audit. Collect data on what feels easy and what feels hard.

– Talk to people who are where you want to be

Not just rich, but calm about money. Ask them what they did in their 20s, 30s, or 40s that made the biggest difference.

Personal finance author Liz Weston often recommends focusing on “the next right move, not the perfect move.” You don’t have to optimize everything — just avoid the big mistakes and keep learning.

—

Resources for Learning: Turn Confusion into Confidence

You don’t need to figure this out alone. There are high‑quality, low‑noise resources that can turn you from anxious to informed.

– Books

– “The Psychology of Money” by Morgan Housel — helps you understand why you behave the way you do with money.

– “Your Money or Your Life” by Vicki Robin — excellent for connecting spending with your values.

– “I Will Teach You to Be Rich” by Ramit Sethi — conversational, practical, especially good for beginners.

– Podcasts

– “Afford Anything” — deep dives into financial independence and smart decisions.

– “ChooseFI” — stories and strategies for building buffers and long-term security.

– “The Stacking Benjamins Show” — light, humorous, but packed with useful interviews.

– Web and courses

– Free budgeting articles and calculators from reputable sources like major banks, non-profit credit counseling agencies, and government financial education portals.

– Low-cost online courses on platforms like Coursera or Udemy about personal finance basics, investing, and money psychology.

Pick one resource and stick with it for a month. Dipping into 20 different opinions in one week only creates overwhelm. Depth beats noise.

—

Bringing It All Together: Your Buffer, Your Rules

You don’t need to become a finance nerd to feel safe. You need:

– A simple budget that shows where your money goes.

– A growing buffer that separates you from the next surprise bill.

– A few habits — automation, weekly check-ins, and small continuous improvements.

Start where you are, with what you have. Maybe that’s $20 a week into a new savings account, or finally downloading a budgeting app and categorizing the last month.

The buffer you’re building is more than money. It’s the confidence to say “I’ll handle it” the next time life gets unpredictable. And that feeling is worth every quiet, consistent step you take today.