Why budgeting is less about numbers and more about control

Budgeting has a reputation problem. Many beginners imagine spreadsheets, restrictions, and guilt. In reality, a basic plan for your money is closer to Google Maps: you tell it where you want to go, it shows you the route, and warns you when you’re drifting off course.

For most people, the goal isn’t to become a finance nerd. It’s to stop worrying if the card will go through, to pay bills on time, and to see savings actually grow. That’s where budgeting for beginners really starts: with clarity, not with complicated math.

Financial planners often say the same thing: your first budget doesn’t have to be perfect, it just has to be honest.

—

Step 1. Get the real numbers (not the ones in your head)

Most people “kind of know” how much they spend. Then they check the actual data and discover they’re off by 20–40%. That gap is exactly where stress, debt, and “where did my money go?” live.

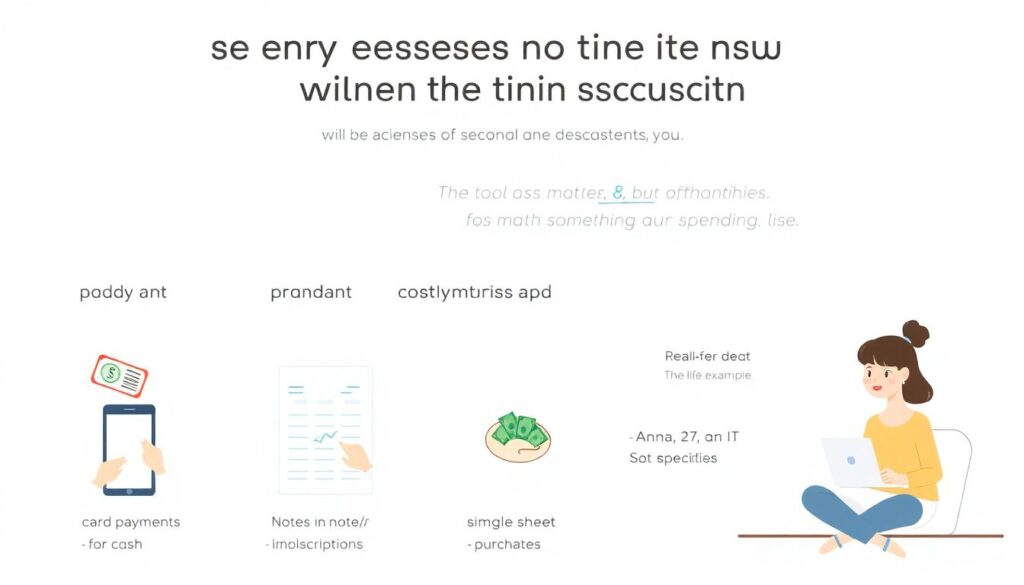

Track 30 days of spending – like a scientist

For one month, track every expense, no exceptions:

– Card payments

– Cash

– Subscriptions

– Random online purchases

You can do it with an app, notes on your phone, or a simple Google Sheet. The tool doesn’t matter; consistency does.

Real-life example

Anna, 27, IT specialist, was sure her main problem was rent. After 30 days of tracking, she discovered:

– Rent: $900

– Groceries: $320

– Eating out and coffee: $410

– Subscriptions and “small stuff”: $95

She wasn’t “bad with money” — she simply underestimated how often she bought food on the go. Just seeing the numbers shifted her behavior without any extreme measures.

—

Technical block: minimal data set for a beginner budget

To build a working beginner budget, you need four groups of numbers:

1. Net monthly income (after taxes and deductions)

2. Fixed expenses (don’t change much month to month)

– Rent / mortgage

– Utilities

– Transport pass, insurance, phone

3. Variable expenses (can be adjusted)

– Groceries, cafes, entertainment, shopping, gifts

4. Financial goals

– Emergency fund

– Debt payments above minimum

– Long-term savings (education, down payment, investments)

You don’t need more categories at the start. Too much detail usually kills motivation.

—

Step 2. Choose a simple structure: 50/30/20 and its real-world tweaks

A popular framework for how to make a personal budget is the 50/30/20 rule:

– 50% of take-home pay → Needs

– 30% → Wants

– 20% → Savings and debt payoff

It’s not a law, it’s a starting benchmark.

How it looks with real numbers

Imagine you take home $2,500 a month.

– Needs (50%): $1,250

– Rent, utilities, basic groceries, minimum debt payments, transport, basic insurance

– Wants (30%): $750

– Restaurants, travel, hobbies, streaming, “fun” shopping

– Savings & debt (20%): $500

– Emergency fund, extra loan payments, investments

For many beginners, especially in big cities, “needs” eat closer to 60–70% of income. That’s normal at first. The point is not to feel guilty, but to see the imbalance and gradually push it in the right direction.

—

Technical block: when 50/30/20 doesn’t fit

Situations where the classic rule is unrealistic:

– High rent region

– Needs: 60–70%

– Wants: 10–15%

– Savings & debt: 15–25%

– Aggressive debt payoff phase

– Needs: 45–55%

– Wants: 5–15%

– Savings & debt: 30–50%

– Student or unstable income

– Focus: build a tiny emergency buffer first ($500–$1,000)

– Treat extra income as “bonus” for savings and debt rather than for lifestyle

Expert recommendation: adjust the percentages, but keep the three buckets. That mental structure is more important than the exact numbers.

—

Step 3. Translate your budget into a monthly action plan

Numbers are theory. Cash flow is practice. The next step is turning goals into what you actually do with each paycheck.

Pay-yourself-first vs “leftover” saving

Most people use the leftover approach:

> “I’ll save whatever is left at the end of the month.”

Behavioral finance research shows this almost never works long-term. Lifestyle spending expands to fill available cash.

The pay-yourself-first approach flips the script:

1. Income hits your account.

2. You immediately move money to:

– Savings

– Extra debt payments

3. You live on what remains.

Even 5–10% saved automatically is better than planning 20% “if nothing unexpected happens.”

—

Technical block: a basic paycheck allocation formula

For every paycheck:

1. Automatic transfers on payday

– X% to savings account (emergency fund or goal)

– Y% to extra debt payments

2. Separate “bill” account (optional but powerful)

– Sum up all monthly fixed bills

– Divide by number of paychecks per month

– Move that amount to a bills-only account each payday

3. Spending account

– What’s left is for daily life and fun

This structure prevents “bill shock” at the end of the month and gives a clear view of what’s actually safe to spend.

—

Step 4. Choose your tools: apps, templates, or simple lists

Tools don’t create discipline, but they can remove friction. The right format depends on your personality more than on “expert rankings”.

For the visual and digital type

Many people prefer using apps instead of spreadsheets. The best budgeting apps for beginners usually share three features:

– Automatic bank sync

– Simple category setup

– Clear overview of “safe to spend” money

Examples of popular app types (not endorsements, just categories):

– Zero-based budget apps: Every dollar is assigned a job. Great for detail-oriented minds.

– Envelope-style apps: Virtual “envelopes” for groceries, fun, transport, etc. Good for impulse control.

– Simple trackers: Just show where money went. Useful at the very start.

—

If you like pen and paper or minimalism

A monthly budget planner template in a notebook or Google Docs can be just as effective. The structure can be as light as:

– Income

– Fixed bills

– Flexible spending categories

– Savings / debt goals

The key is that you look at it before you spend, not only afterward.

—

Technical block: must-have sections in any template

When you create or download a template, check that it includes:

1. Start-of-month balances (checking, savings, debt totals)

2. Planned amounts by category

3. Actual spending fields

4. Difference (planned vs actual)

5. Notes for explaining big deviations (car repair, medical bill, etc.)

This “difference” line is where learning happens. Without it, a budget is just a list.

—

Step 5. Prioritize protection: emergency fund and debt

A worry-free financial life doesn’t start with investing. It starts with not being wiped out by one surprise.

How much is “enough” for an emergency fund?

Most experts recommend:

– Starter level: $500–$1,000

– Buffer for small emergencies: car issues, medical co-pays, urgent repairs

– Core level: 3–6 months of essential expenses

– Rent, utilities, groceries, transport, minimum debt payments

If your job is unstable or you’re self-employed, move toward the higher end (6 months or even more).

Practical sequence for beginners

1. Save first $500–$1,000 as fast as possible (temporary side gigs, selling unused things, pausing some wants).

2. Shift extra focus to high-interest debt (credit cards, personal loans above ~15–20% APR).

3. After that, grow the emergency fund toward 3–6 months.

—

Technical block: simple debt payoff comparison

Two popular approaches:

1. Debt avalanche (mathematical)

– Pay extra on the highest interest rate first.

– Saves the most money over time.

2. Debt snowball (psychological)

– Pay extra on the smallest balance first.

– Builds quick wins and motivation.

Experts increasingly suggest a hybrid:

– Minimums on all debts

– Extra money to the highest interest among your smaller balances first

– Once a few small, expensive debts are gone, attack the big ones

—

Step 6. Start small and automate behavior, not willpower

The biggest budgeting mistake beginners make is trying to change everything at once: no coffee, no eating out, no fun, gym five times a week, $1,000 saved every month. It usually collapses within weeks.

Build “must-win” habits, not heroic challenges

Pick 2–3 low-friction changes:

1. Move $50–$100 to savings automatically on payday.

2. Set a realistic weekly limit for one tricky category (e.g., dining out or delivery).

3. Review your accounts for 10 minutes every Sunday.

Over three months, these mild adjustments change your trajectory more than one month of strict austerity followed by burnout.

Real-life example

David, 31, with a $3,000 take-home income, didn’t want a complicated system. He set:

– Automatic $150 transfer to savings

– $80/week cap on restaurants

– A simple note in his calendar: “Money check – Sunday 6 p.m.”

After 6 months:

– Emergency fund: from $0 to $1,100

– Credit card debt: from $3,200 to $2,350

– Subjective anxiety about money: “Dropped from 9/10 to about 4/10,” in his words.

—

Technical block: basic weekly check-in script

Once a week, go through:

1. Check balances

– Checking, savings, main debts

2. Review transactions

– Any surprises? Any categories getting out of control?

3. Adjust next week

– Reduce some discretionary categories if needed

– Or move a bit extra into savings if you’re under budget

4. Note one insight

– “I always overspend on weekends.”

– “Groceries are cheaper if I go with a list.”

This reflection loop turns raw numbers into behavior change.

—

Step 7. Beginner-friendly saving strategies that actually work

Saving isn’t just about not spending. It’s about designing your environment so the default option is the one that helps you.

How to start budgeting to save money without feeling deprived

A few proven tactics:

1. Pre-decide your “fun money”

– Give yourself a specific monthly amount for guilt-free spending.

– When it’s gone, that’s it. No shame attached.

2. Create “speed bumps” for impulse buys

– Remove saved cards from 1-click shopping sites.

– Add a 24-hour rule for purchases above a set amount (e.g., $100).

3. Use separate accounts with names

– “Emergency fund,” “Travel 2026,” “New laptop.”

– Research shows labeled accounts increase savings rates because every transfer feels like progress toward something concrete.

—

Technical block: starter savings targets

As a beginner, you can use these ballpark numbers:

– If you have high-interest debt

– Starter goal: 5–10% of income to savings, 10–20% to extra debt (if possible)

– If debt is low or moderate

– 15–20% total toward savings and investments over time

– If income is very tight

– Start with 1–3% just to build the habit and prove to yourself it’s possible

The habit and automation matter more than the initial amount.

—

Step 8. Using apps and templates without becoming a slave to them

Technology should reduce decision fatigue, not create more tasks.

When to lean on apps

Consider using an app if:

– You hate manual entry

– You have multiple accounts and cards

– You often forget upcoming bills

Then a simple budgeting tracker that pulls in your transactions and shows category totals can make staying on track much easier.

But if you find yourself spending more time tweaking categories than using the budget to decide anything, simplify. The best tool is the one you’ll still be using in 6 months.

—

When a minimal template is enough

If your financial life is relatively simple — one main income, one card, a few bills — a one-page monthly budget planner template can carry you a long way:

– At the start of the month: set planned amounts.

– Mid-month: quick check-in, adjust if needed.

– End of month: fill actual amounts, note lessons, roll into next month.

This keeps budgeting light but intentional.

—

Expert recommendations for a low-stress money system

Let’s condense the analytical approach into specific, expert-backed moves.

1. Focus on cash flow before investment returns

Most certified financial planners agree: for beginners, the priority is:

1. Positive monthly cash flow

2. Emergency fund

3. High-interest debt reduction

Only after that do investment choices start to seriously matter. Without this foundation, even good investments can be wiped out by one emergency.

—

2. Define what “worry-free” actually means for you

For one person, it’s “I can pay my bills on time and save $200 a month.”

For another, it’s “I can handle losing my job and live for 6 months without panic.”

Write your version down. Then adjust your budget to move you in that direction, step by step.

—

3. Make the budget flexible on purpose

Experts often recommend treating the budget as a “living document,” not a contract:

– You’re allowed to move money between categories.

– Overspending in one category is a signal, not a failure.

– If income changes, you update the plan — that’s not breaking the budget, that is budgeting.

Rigidity breaks. Flexibility survives life.

—

4. Use a 90-day experiment mindset

Instead of “I must do this forever,” treat your first attempt as a 3‑month experiment:

1. Month 1: Observe and guess (rough categories, see where you miss).

2. Month 2: Adjust based on reality (increase underestimates, trim where possible).

3. Month 3: Stabilize (lock in a version that feels challenging but not suffocating).

After those 90 days, you’ll know more about your money habits than in the last few years — and you’ll have proof that you can change them.

—

Putting it all together

To create a calm, beginner-friendly money system:

1. Collect real numbers for 30 days.

2. Choose a simple structure (like 50/30/20, adjusted to your reality).

3. Set up automatic transfers right after payday.

4. Use one tool (an app or a simple template) consistently, not perfectly.

5. Build a starter emergency fund, then target high-interest debt.

6. Review weekly, adjust without drama, and treat everything as data.

Budgeting for beginners isn’t about being perfect with money. It’s about designing a system where the default is progress, and worry slowly fades into the background because you know, in concrete numbers, that you’re going to be okay — and, step by step, better than okay.