Why budgeting feels scary (and how to reframe it)

Most beginners picture budgeting as a strict diet for money: all rules, zero joy. That mindset kills motivation fast. Try another angle: a budget is simply a map of where your cash already goes and where you’d *rather* send it. Before worrying about how to start a budget and save money, accept one idea: clarity comes before control. For the first month, don’t “fix” anything. Just track. This low‑pressure phase lowers anxiety, reveals leaks, and turns vague guilt into specific, solvable problems. Confidence grows from data, not from guesswork.

Real case: from paycheck panic to calm plan

Emma, 27, lived in constant overdraft despite a decent salary. She swore she had “no fat to cut”. For 30 days she logged every card and cash payment in a simple monthly budget planner for beginners: four categories only—Needs, Wants, Debts, Goals. The surprise? Food delivery and “tiny” online purchases ate almost 30% of her income. Instead of banning them, she set a fixed fun allowance and automated an extra $150 to debt. Three months later, overdraft fees vanished and her stress dropped more than her spending.

Non-obvious move: budget for your weak spots, not your ideals

Many guides push you toward the perfect 50/30/20 split straight away. For most beginners that’s fantasy. Start from your real habits and work backwards. If you constantly overspend on socializing, don’t slash it to zero; cap it intentionally and cut in areas you care about less. One of the strongest budgeting tips to pay off debt fast is to protect emotional “must-haves” in small doses. That way you can redirect bigger chunks toward loans without triggering a rebound binge that wipes out your progress.

Real case: debt avalanche with a twist

Carlos had five credit cards and felt paralyzed. A coach suggested the classic avalanche: pay highest interest first. But emotionally, he needed quick wins. They combined methods: he listed debts by balance and by rate. First, he wiped out one tiny card for momentum, then fully switched to the highest‑interest one. That hybrid method felt both smart and satisfying. In eight months he cleared three cards. The lesson: formulas are great, but your psychology pays the bills. Adjust strategy until you can stick with it on a bad week.

Alternative ways to track: not just spreadsheets

If spreadsheets make your eyes glaze over, don’t force them. There are best budgeting apps for beginners that use visuals, alerts, and automatic categorizing. But even those can feel heavy. An underrated alternative is the calendar method: write income and major bills on a calendar, then add expected daily spending. Seeing cash flow across days, not just in abstract categories, helps you avoid the “rich on payday, broke two weeks later” cycle. You’re still budgeting—just mapping time and tension instead of obsessing over perfect categories.

Simple starter system: the 4-bucket approach

To avoid overwhelm, try this ultra simple monthly budget planner for beginners built from four “buckets”: Essentials, Fun, Debts, Future. 1) Estimate your after‑tax income. 2) Assign money to essentials first: housing, food, transport, minimum payments. 3) Decide a realistic Fun number you won’t feel guilty about. 4) Split the rest between extra debt payments and savings. 5) Automate everything you can. This isn’t fancy, but it’s sticky. Once it runs for a few months, refine the percentages instead of redesigning the whole system.

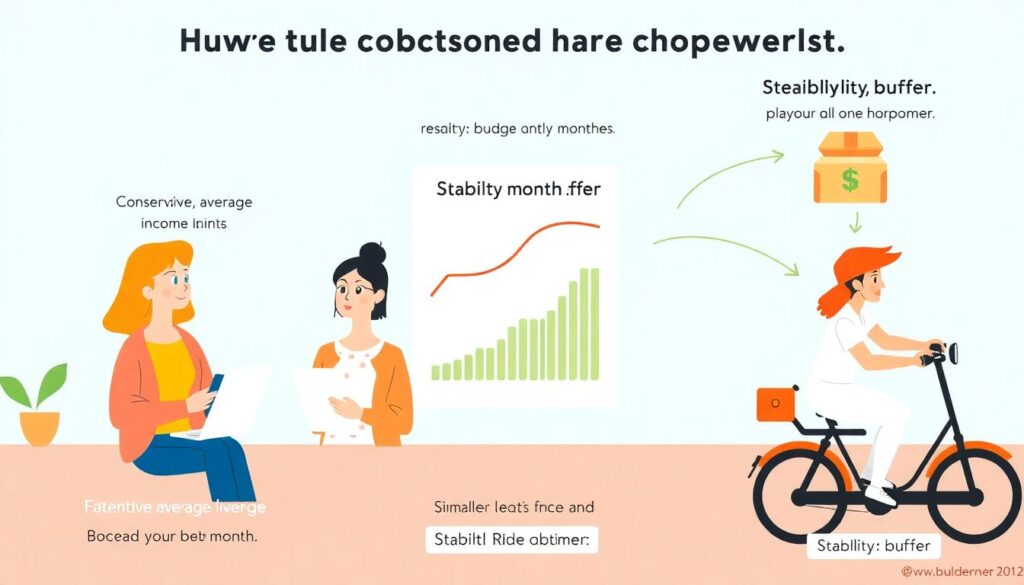

Non-obvious solutions for irregular income

Freelancers and gig workers often think budgeting “doesn’t work” for them. It can—if you flip the logic. Base your plan on a conservative average, not your best month. Create a “stability buffer” account with one simple rule: big months feed it, lean months withdraw from it. Treat that buffer like a personal paycheck generator. This way you still enjoy clarity and a steady budget, while your actual income waves up and down in the background. The budget becomes a shock absorber instead of a monthly guessing game.

Learning faster: use other people’s brains

You don’t need to reinvent every wheel. Short personal finance courses for budgeting beginners can compress years of trial and error into a few hours, especially around topics like debt strategies, negotiating bills, or setting realistic savings goals. Look for courses that include worksheets or live Q&A so you can adapt advice to your situation. Pair a course with one concrete action per week—renegotiate a bill, adjust categories, or automate a transfer. Education only builds confidence when it changes what happens to your money on payday.

Pro-level hacks you can borrow on day one

You don’t need to be an expert to use “advanced” moves. First, create default decisions: set automatic transfers the day after payday so saving doesn’t rely on willpower. Second, separate accounts by job: one for bills, one for variable spending, one for goals. That visual separation reduces mistakes. Third, run a five‑minute weekly “money check‑in”: glance at balances, upcoming bills, and one thing to tweak. These tiny routines are what seasoned budgeters rely on more than complicated rules or endless spreadsheets.

Real case: turning clarity into long-term confidence

Nina and Alex constantly argued about money. Instead of another fight, they set up a shared “money night” every Sunday. Together they checked their app, chose one expense to trim, and one treat to keep. As their buffer grew, they noticed something: arguments dropped because decisions weren’t made in panic anymore. Their clarity—knowing what they could and couldn’t afford—slowly became confidence. That’s the real aim of budgeting: not perfection, but fewer surprises, fewer regrets, and more moments where you can say “yes” without that sinking feeling.