Most budgeting advice sounds like it was written by a spreadsheet, not a human. Let’s fix that. You don’t need to become an accountant; you just need a simple, repeatable system that tells you what your money should do before it disappears. Below is a practical, realistic, step by step monthly budget plan designed for real life, with room for mistakes, laziness, and unexpected bills.

—

Why budgeting for beginners usually fails

Most people quit budgeting not because they “lack discipline”, but because the system they tried was statistically doomed. Surveys in the US and Europe show that more than 60–65% of new budgeters drop the process within three months. The main cause is cognitive overload: 40+ spending categories, rigid rules, and moral pressure to “cut coffee”. In behavioural economics this is classic decision fatigue; the brain starts skipping tracking, then the whole system collapses. A sustainable framework for budgeting for beginners must behave more like a navigation app than a ledger: minimal inputs, continuous feedback, automatic course correction. Think of it as a cash‑flow operating system, not a guilt diary about lattes and takeout.

Short version: if your budget feels like homework, you’ll abandon it. If it feels like a dashboard, you’ll actually use it.

—

A simple architecture: three buckets, not thirty

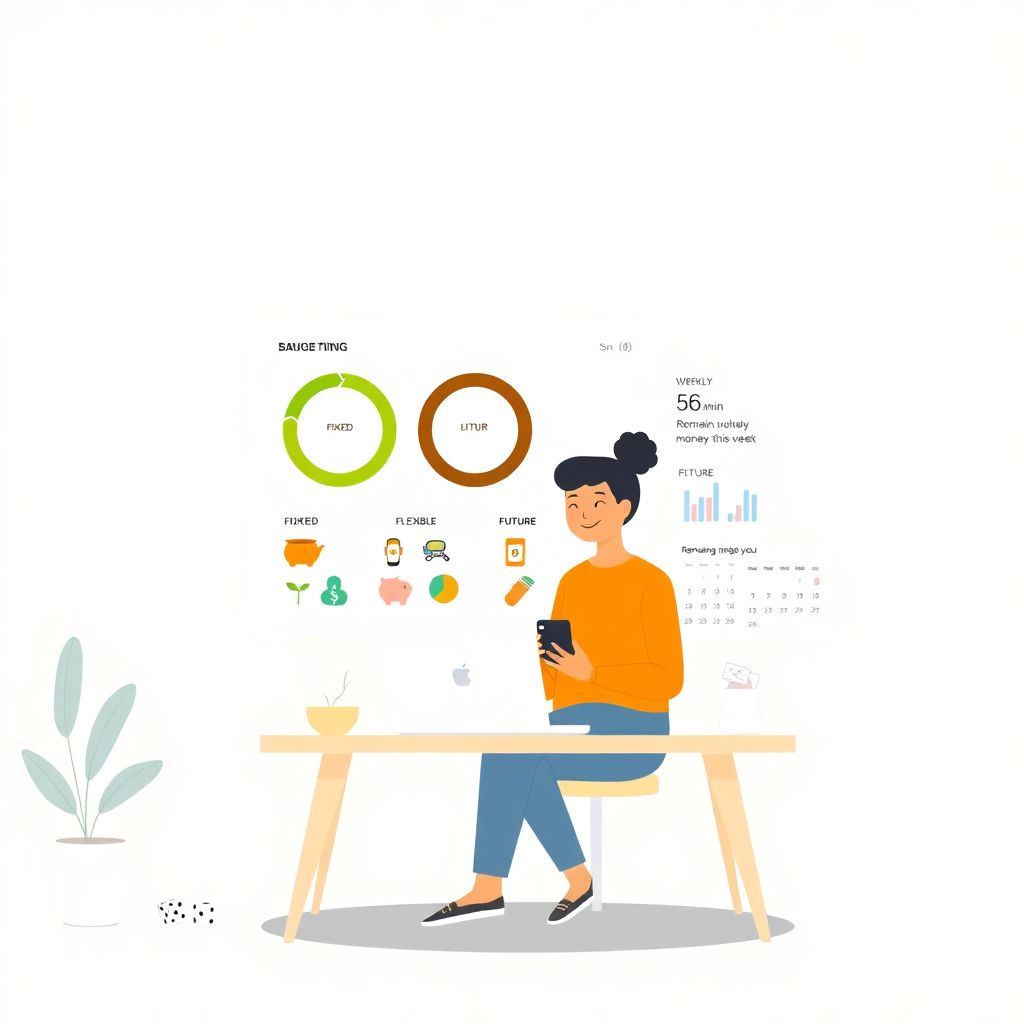

Core structure of a personal budget planner for beginners

Instead of slicing your life into dozens of micro‑categories, use just three buckets: Fixed, Flexible, and Future. This minimal structure mirrors how macroeconomists think about household consumption vs. investment, but in plain English. Fixed = everything that keeps your life running and rarely changes month to month (rent, utilities, transport pass, insurance, debt minimums). Flexible = food, fun, shopping, random Amazon orders. Future = emergency fund, big goals, investing, debt overpayments. A personal budget planner for beginners built on these three flows is mathematically sufficient to capture 95% of consumer spending patterns without drowning you in detail. The trick is that you only need precise tracking inside the Flexible bucket; Fixed and Future are mostly pre‑scheduled, saving you daily decision energy and drastically reducing the chance you’ll quit.

Your first nonstandard move: permit yourself not to track “everything”, only what actually moves.

—

How to create a budget plan that survives real life

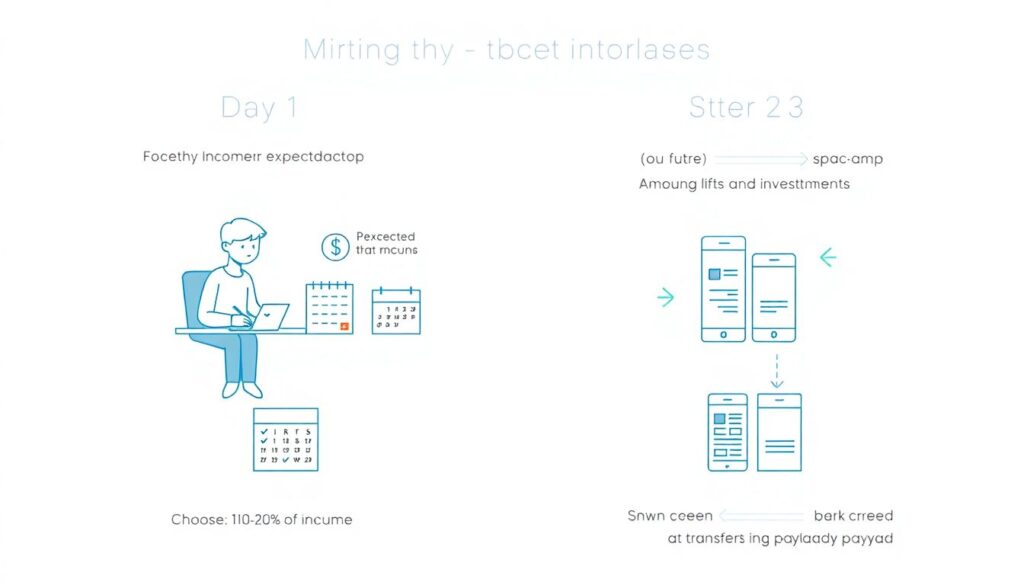

Step 1: Start from zero, not from your bank history

Instead of obsessing over the last three months of transactions, start forward‑looking. To understand how to create a budget plan that works, ask just four questions: what do you reliably earn next month, what absolutely must be paid, what would you like to keep doing, and what do you want money to change long‑term? This future focus reduces shame and anchors you in planning, not post‑mortem analysis. Then, roughly allocate your income: Fixed first, Future second, Flexible gets the leftovers. Counter‑intuitively, this “pay Future before Fun” order maps to the pay‑yourself‑first principle known from corporate finance, but here it’s applied to your household balance sheet. You’re not “restricting” yourself; you’re simply deciding what portion of your future you want to pre‑buy right now.

You can refine historical data later; the first version just needs to be directionally correct, not perfect.

—

Step 2: A step by step monthly budget plan you can run in 15 minutes

Here’s the monthly cycle, stripped down. On Day 1, write down your expected income and lock in Fixed costs; schedule them as automatic payments where possible. Next, choose a flat number for Future—say 10–20% of income—even if that feels tiny; automate transfers to savings or investments on payday. Whatever remains becomes your Flexible pool for the month. Then divide that Flexible amount by the number of remaining weeks and treat each week like a mini‑budget. This is your core step by step monthly budget plan: one monthly decision on structure, four weekly check‑ins of 5 minutes each. Behaviourally, weekly cycles align with how people perceive time and control impulses; you’re never “failing the month”, just recalibrating the next week. This transforms budgeting from a moral referendum into a routine parameter update, similar to adjusting a thermostat.

The real innovation is shrinking the planning horizon so your brain can actually see the finish line.

—

Tools and tech: using the best budgeting apps for beginners intelligently

Why apps fail—and how to flip them

Most software throws charts at you without changing behaviour. To actually help, the best budgeting apps for beginners must do three jobs: enforce the three‑bucket logic, show you only the decisions that matter this week, and send context‑aware alerts before, not after, you overspend. Recent market data suggests fintech budgeting and savings apps will grow by over 20% annually this decade, but churn rates remain brutally high because interfaces are designed for data enthusiasts, not stressed users. Your unconventional move is to use apps as “guardrails”, not as your primary brain. Configure just three top‑level groups, disable most non‑critical notifications, and highlight only one metric on the home screen: remaining Flexible money for the current week. Any app that can’t be bent to this workflow is wasting your attention, no matter how pretty the graphs look.

In short, let the app handle arithmetic; you handle priorities.

—

Economic context: why your micro‑budget matters in the macro picture

At scale, millions of small budgets shape demand in entire industries. When households systematically redirect even 5% of their spending from unplanned consumption to Future buckets, the aggregate effect resembles a structural rise in national savings and investment rates. Economic models show that such shifts dampen volatility in discretionary sectors (hospitality, fast fashion) and channel capital toward financial services, fintech, and long‑term asset markets. Central banks already monitor household balance sheet health as a leading indicator of crisis resilience; widespread adoption of robust household cash‑flow management could statistically reduce default probabilities and smooth recession shocks. For you, this translates into lower systemic risk around your job, your mortgage rate, and your pension. For companies, it forces a pivot from impulsive, ad‑driven sales to subscription‑based and value‑retention models, because better‑budgeting consumers are harder to manipulate with one‑click purchases.

Your small spreadsheet is, quietly, a political and macroeconomic instrument.

—

Forecasts and the future of personal budgeting

From static budgets to adaptive “money autopilots”

Analysts expect AI‑assisted financial planning tools to become standard inside banking apps within the next 5–7 years. Instead of just tracking, they will simulate scenarios: “If you keep your current lifestyle, you’ll delay home ownership by 4.3 years.” This moves personal finance from bookkeeping towards predictive analytics. In this environment, a robust framework for budgeting for beginners becomes even more important: if your underlying categories are chaos, algorithmic advice will amplify noise. We’re likely to see dynamic budgets that adjust allocations daily based on real‑time transaction streams and even local price indices. Yet behavioural evidence suggests humans still need clear, simple mental models. So the winning systems will combine an invisible algorithmic layer that auto‑tunes numbers with a visible three‑bucket interface your brain can grasp in seconds. You’ll feel like you “set the strategy” while the machine handles micro‑adjustments.

The future of budgeting is less about more features and more about frictions that nudge you gently but relentlessly toward your stated goals.

—

Nonstandard tweaks to keep your budget alive

Gamify, randomize, and deliberately “waste” some money

Here are a few unconventional, yet technically grounded tweaks. First, introduce a “chaos buffer” inside your Flexible bucket: an explicit line item for miscalculations and forgotten expenses. Behaviourally, this converts budget leaks into expected variance, which makes you less likely to abandon the system after one bad week. Second, randomize micro‑rewards: when you come in under your weekly Flexible limit, roll a die to decide how much of the leftover goes to Fun next week versus Future; that bit of randomness has been shown in experiments to increase engagement in repetitive tasks. Third, create a small, sacred “waste budget” for guilt‑free frivolity; paradoxically, clearly labelled indulgence reduces unplanned splurges by satisfying the brain’s need for autonomy. These tactics aren’t about being quirky—they are about engineering a budget that accommodates human psychology instead of fighting it.

Your plan doesn’t have to be strict; it has to be survivable.

—

Putting it all together without burning out

When you assemble the pieces, you get a lean system: a three‑bucket structure, a monthly and weekly loop, light use of tech, and a few psychological hacks. That’s essentially a personal operating manual for money—a personal budget planner for beginners that can evolve into an advanced framework without ever becoming unreadable. To start today, you don’t need to clean your transaction history or build elaborate spreadsheets. Take your next expected paycheck, assign Fixed, pick a Future percentage, and treat what’s left as this week’s Flexible pool. Capture the numbers in any app or notebook and run the loop for a single month. If it feels clunky, adjust the ratios, not the whole architecture. Over time, this simple design will give you the one thing most financial advice never delivers: a feeling that you are quietly but decisively moving from reacting to your money to directing it.