Why Automatic Transfers Are the Easiest “Set It and Forget It” Money Move

Let’s be honest: most people don’t “forget” to save — they just don’t get that far. The money hits the account, bills and spontaneity win, and whatever is “left over” is… nothing.

That’s exactly why automatic transfers to savings exist. You move the decision from “Do I feel like saving this month?” to “It happens whether I remember or not.”

According to U.S. Federal Reserve and major bank surveys from 2021–2023, people who automate savings are about twice as likely to hit their savings goals compared to those who move money manually. Over the same period, the U.S. personal savings rate hovered between roughly 4–10% of income, but people using automatic transfers often report saving 10–15% consistently. The behavior shift is real.

This guide walks you through the beginner-friendly, non-boring way to set everything up — plus a few pro tricks you rarely hear about.

—

What “Automatic Transfers for Savings” Actually Mean (In Real Life)

The simple version

You tell your bank or app:

“Every time money comes in (or every month on this date), move X to that savings account.”

That’s it. The magic is in the consistency.

In practice, an online banking automatic transfer to savings usually looks like:

– You get paid on the 1st and 15th.

– On the 2nd and 16th, your bank automatically sends, say, $100 from checking to savings.

– You never log in, never tap anything, and it just… happens.

Why this matters more than “being disciplined”

Between 2021 and 2023, Bankrate and similar surveys repeatedly found that over half of Americans couldn’t cover a $1,000 emergency in cash. At the same time, employer benefit reports show that workers who enroll in automatic retirement contributions are far more likely to keep saving long term than those who need to opt in every time.

Same brain. Same psychology.

When saving is manual, you negotiate with yourself. When it’s automatic, there is nothing to negotiate.

—

Step Zero: Decide What You’re Actually Saving For

Give every transfer a job

Before you touch your banking app, pick one concrete goal:

– $1,000 starter emergency fund

– 3–6 months of expenses

– A trip in 6 months

– A “buffer” so you’re not sweating every bill cycle

Vague goals like “I should save more” don’t survive contact with a sale or a bad day.

Now translate that goal into a monthly number. Example:

– You want $1,200 in 12 months → $100/month

– Paid twice a month → $50 from each paycheck

That’s the number you’ll use when deciding how to set up recurring transfers to savings in your bank.

—

How to Set Up Automatic Transfers in Your Bank (Without Overthinking It)

Basic automatic savings account setup: the 5‑minute version

Most banks follow roughly the same flow:

1. Log into your online or mobile banking.

2. Go to “Transfers” or “Move Money.”

3. Choose From: Checking → To: Savings.

4. Select “Repeat”, “Recurring,” or “Schedule.”

5. Pick how often (every paycheck, weekly, or monthly) and the start date.

6. Hit confirm. You’ve done an automatic savings account setup.

If you’re paid irregularly (freelance, gig work), weekly transfers often work better than trying to line up with “paydays” that shift.

Real case: how Anna stopped raiding her savings

Anna, 29, freelance designer, had a classic problem: every time she manually moved money into savings, she moved it back out two weeks later.

Her fix was surprisingly small:

– She opened a separate online savings account at a different bank with no debit card.

– She set a weekly transfer of $40 instead of a big monthly chunk.

– In three years (2021–2023), she averaged around $160/month saved almost without noticing.

Because the money left in small, frequent bites and wasn’t instantly visible in her main app, she stopped reversing the transfer.

—

Choosing Where to Park Your Savings (And Why the Bank Matters)

Not all banks are equal for automation

You don’t need the “best bank on Earth,” but some are clearly the best banks for automatic transfers to savings:

– Clean, simple app with easy scheduling

– No monthly fees for having a savings account

– Competitive interest rate (many online banks paid notably higher rates than big brick‑and‑mortars from 2021–2023)

– Fast transfers between checking and savings (same day or next day)

If your current bank makes it painful to open a new savings account or schedule a transfer, that friction will kill your momentum. In that case, opening a separate high‑yield online savings account can pay off very quickly.

Short checklist before you stick with a bank

Ask yourself:

1. Can I open multiple savings “buckets” easily?

2. Does the app make recurring transfers obvious, not buried in menus?

3. Are there minimum balance requirements that might bite me?

If you’re annoyed after 3 minutes in the app, that’s a red flag.

—

Automatic Savings Apps for Beginners: When the Bank Isn’t Enough

Apps that save “behind your back” (in a good way)

Over the last few years, a wave of automatic savings apps for beginners has popped up that sit on top of your normal bank account. Many of them:

– Scan your spending and income

– Predict what you can safely save

– Move small amounts (like $2–$10) several times a week

From 2021–2023, user reports and fintech disclosures showed millions of people collectively saving billions of dollars through these “micro‑saving” apps, with many users saying it was the first time they’d ever kept more than a few hundred dollars in savings.

These apps are especially helpful if:

– Your income is irregular

– You hate budgeting but want progress

– You’re anxious about moving “too much” and bouncing payments

Hidden downside nobody sells you on

Some apps charge subscription fees or keep your money in accounts that pay low or no interest. If you’re saving $50/month and paying $5/month for the app, you’re handing over 10% of your progress.

Rule of thumb:

If an app helps you start saving and break the “0 in savings” curse, it can be worth the fee for a while — just don’t forget to reassess once your habit is solid.

—

Non‑Obvious Ways to Automate Savings Without Touching Your Bank (Yet)

Payroll-level automation: the move most people skip

The most powerful automation often happens before your paycheck hits your checking account.

Ask your employer if you can:

– Split direct deposit between two accounts (checking + savings)

– Send a flat amount (e.g., $150) or a percentage (e.g., 10%) straight to savings

Because the money never appears in checking, you’re not tempted to spend it. This “pay yourself first” method has been a core feature of retirement plans for decades — and it works just as well for regular savings.

Using “round‑ups” without relying on marketing hype

Some banks and apps round every purchase to the nearest dollar and send the difference to savings. Example: spend $7.30 → $0.70 goes to savings.

Round‑ups:

– Won’t fully fund big goals

– But they can add $10–$50/month quietly, based on average card usage data from large banks in 2022–2023

Treat round‑ups as extra, not your main strategy. They create small wins that keep you emotionally engaged.

—

Real People, Real Fixes: 3 Short Case Studies

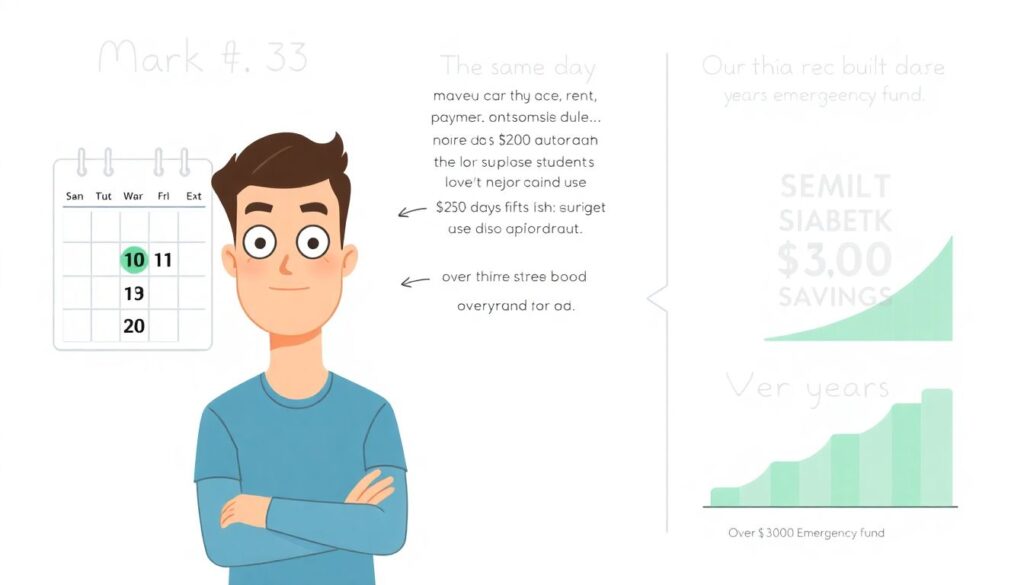

1. The “always overdrafting” situation

Mark, 33, set a $200 transfer the same day his rent, car payment, and student loan hit. Result: surprise overdrafts.

His fix:

– Move his recurring transfer to three days after his major bills

– Drop it to $120 at first, then increase gradually

In three years, he built a $3,000 emergency fund and stopped paying overdraft fees — pure profit.

2. The “too many goals, no progress” problem

Sophia tried to save for travel, a new laptop, and emergencies all at once. She opened three sub‑accounts and set tiny transfers to each.

It looked organized but felt pointless.

Her fix:

1. She paused two goals and focused only on the emergency fund.

2. Set a single, bigger transfer to that one account.

3. When it hit $1,500, she split the transfer between all three again.

Completion bias matters. Seeing one account actually hit a target beats watching three limp along forever.

3. The “late to the game” restart at 45

Michael, 45, had almost no savings after helping family and dealing with medical bills. He assumed he was “too late.”

He started with:

– A small weekly automatic transfer of $25

– A rule: increase the transfer by $10 every time he got a raise or finished paying a debt

From 2021–2023, he managed to ramp up to $75/week, building over $10,000 in liquid savings. The key wasn’t the amount at the beginning — it was the automatic escalation over time.

—

Alternative Methods: When Standard Recurring Transfers Don’t Fit

Income-based automation for freelancers and gig workers

If your income is all over the place, fixed monthly transfers can be risky. Instead:

– Save a percentage of each incoming payment, not a fixed dollar amount. For example, 5–15% of every deposit.

– Some banks and apps let you set automation rules like: “Every deposit over $300 → send 10% to savings.”

This naturally scales with busy and slow months.

Goal‑triggered “lump sum” transfers

Not everyone likes money disappearing quietly in the background. Another approach:

1. Track your monthly expenses for 2–3 months.

2. Every time your checking account ends a month above a certain threshold (say, $1,500), automatically move everything above that to savings.

Some people find this more satisfying because they see a big chunk move at once.

—

Advanced Tricks & Pro‑Level Hacks (Still Beginner‑Friendly)

1. Use “friction” strategically

You want easy in, harder out:

– Easy to move money into savings

– Slightly annoying to move it out

How to do that:

1. Keep your main checking and daily card with Bank A.

2. Open a high‑yield savings account with Bank B.

3. Set an automatic transfer from A → B.

4. Don’t order a debit card for Bank B.

Now, transferring money back takes an extra day or two. That delay protects you from impulse raids on your savings.

2. Pair automation with alerts (instead of anxiety)

Set up app notifications so you get:

– An alert when your automatic transfer runs

– A low‑balance warning on your checking account

This combo lets you avoid overdrafts without constantly checking your balance. If you see the low‑balance alert too often, that’s your signal to nudge the transfer down slightly — not to cancel it outright.

3. Layer accounts by time horizon

Once your basic transfer is humming:

1. Keep your emergency fund in a high‑yield savings (quick access).

2. Put near‑term goals (6–24 months) in separate goal‑based savings accounts or “buckets.”

3. For anything beyond 3–5 years, look at long‑term investment accounts rather than just savings.

Your automation then becomes a portfolio of small autopilots, each doing one specific job.

—

Common Mistakes Beginners Make (And How to Avoid Them)

Mistake #1: Starting too big, quitting entirely

People often commit to $300/month because it “feels serious,” then cancel after one tight month.

Better path:

– Start with something almost laughably small ($20/week).

– Add $5–10 every few months or after every raise.

Behavior research from 2021–2023 on saving and retirement contributions shows that gradual increases dramatically improve long‑term participation rates.

Mistake #2: Relying only on apps and ignoring the big picture

An app rounding up your coffee purchases won’t replace a basic plan. Use tools, but still answer:

– What’s my priority goal for this year?

– How much do I want to save per month toward it?

– Where is that money going?

Mistake #3: Never revisiting your setup

Your life in 2021 wasn’t your life in 2023 — and 2025 will be different again. Review your automatic transfers at least once a year:

– New income level? Increase transfers.

– New recurring bills? Adjust timing or amount.

– Goal reached? Redirect that transfer to the next goal.

Automation is a system, not a prison.

—

Putting It All Together: A Simple 30‑Day Action Plan

Your next four weeks, in order

1. Day 1–3: Pick one goal and a number.

Decide what you’re saving for and how much you want per month. Break it into per‑paycheck or weekly amounts.

2. Day 4–7: Do a basic automatic savings account setup.

Use your bank’s app to schedule a recurring transfer. Even if it’s just $10/week, get the system running.

3. Day 8–14: Add one non‑obvious tweak.

– Ask HR about splitting direct deposit, or

– Open a separate high‑yield savings account and redirect the transfer there.

4. Day 15–21: Test and adjust.

Watch your checking balance. If it’s tight, lower (don’t cancel) the transfer or move the date slightly.

5. Day 22–30: Consider an extra tool.

Explore automatic savings apps for beginners if your income is irregular, or if you want micro‑savings on top of your main transfer.

By the end of a month, you’ll have gone from “I should really save more” to having a functioning, personalized system that quietly moves you toward your goals.

—

Final Thought: Automation Is a Money Habit You Build Once

You don’t need perfect willpower, a financial degree, or a six‑figure salary to save. You need:

– One clear goal

– One automatic transfer

– Occasional small tweaks

Whether you use your bank’s online banking automatic transfer to savings feature, a separate high‑yield account, or a mix of tools, the idea is the same: remove daily decisions from the process.

Set it up once. Let it run. Then let your future self enjoy the results.