Understanding Smart Budgeting in 2025

Why budgeting in 2025 is not what it was 10 years ago

If your parents kept their budget in a paper notebook, you’re living in a different universe. In 2025, money management is tightly связана with apps, AI recommendations, instant bank notifications and subscriptions that quietly renew in the background. According to recent U.S. and EU surveys, roughly 55–60% of adults still live paycheck to paycheck, yet downloads of finance apps have grown by more than 150% over the last five years. People clearly want control, but they also need systems that fit modern life — fast payments, side hustles, buy-now-pay-later, and volatile prices.

Smart budgeting is essentially “budgeting plus technology plus behavior science”. It’s not just about writing down expenses. It’s about using smart budgeting tools for managing money that help you notice patterns, automate decisions and reduce the number of willpower-heavy moments in your month.

What “smart” really means in smart budgeting

At its core, smart budgeting combines three things: clear numbers, automation and feedback. You see where the money goes, you set rules so some decisions happen automatically, and you get regular nudges when you drift off track.

In other words, a smart budget does part of the thinking for you.

Step-by-step: building your first smart budget

From zero to a working plan

If you’ve never budgeted, staring at a spreadsheet can feel like learning a new language. That’s why it helps to think in stages. When people search for how to start a personal budget step by step, what they really need is a minimal, realistic system that survives more than two weeks — not a “perfect” one.

Here’s a simple progression that usually works for beginners:

– Stage 1: Awareness. Track where your money actually goes for 30 days. No judgment, just data.

– Stage 2: Limits. Set rough spending caps for the big categories (housing, food, transport, debt, fun).

– Stage 3: Automation. Put bills, savings and debt payments on autopilot where possible.

– Stage 4: Optimization. After 2–3 months, start trimming leaks and adjusting goals.

Most people try to jump straight to Stage 4 and burn out. Smart budgeting slows you down at first, then speeds you up as the system takes over more of the routine.

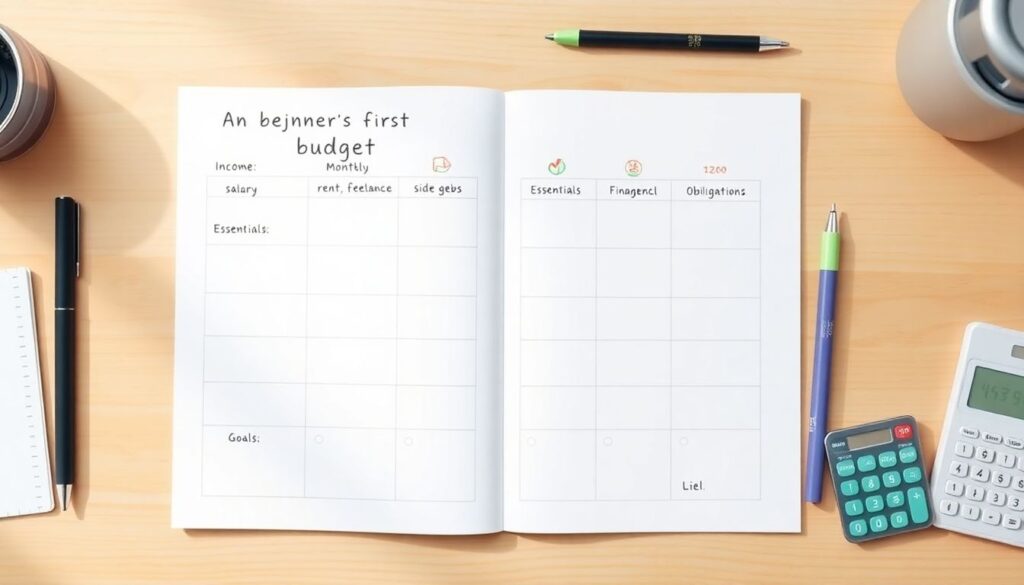

What a beginner-friendly monthly budget looks like

Your first monthly budget planner for beginners doesn’t need 30 categories. Five to eight is enough:

– Income (salary, freelance, side gigs)

– Essentials (rent, utilities, groceries, transport)

– Financial obligations (debt, insurance, taxes)

– Goals (emergency fund, big purchases, investments)

– Lifestyle (eating out, subscriptions, hobbies, travel)

That’s it. You can always split “Essentials” into more detail later if you enjoy that level of control, but simplicity keeps you actually using the system.

Tools: from notebooks to AI-powered apps

Choosing your first budgeting tool

You don’t have to start with software. Some people genuinely do better with pen and paper for the first month because it forces them to pay attention. But because banks, digital wallets and subscriptions are all online, digital tools quickly become more practical.

In 2025, the best budgeting apps for beginners tend to share a few traits: automatic bank syncing, clear visual summaries, simple goal-setting and built-in education (short tips, alerts, tiny “lessons” instead of huge manuals). Many also now include AI-based categorization, which significantly reduces the boring part — labeling each transaction.

What counts as a “smart” tool

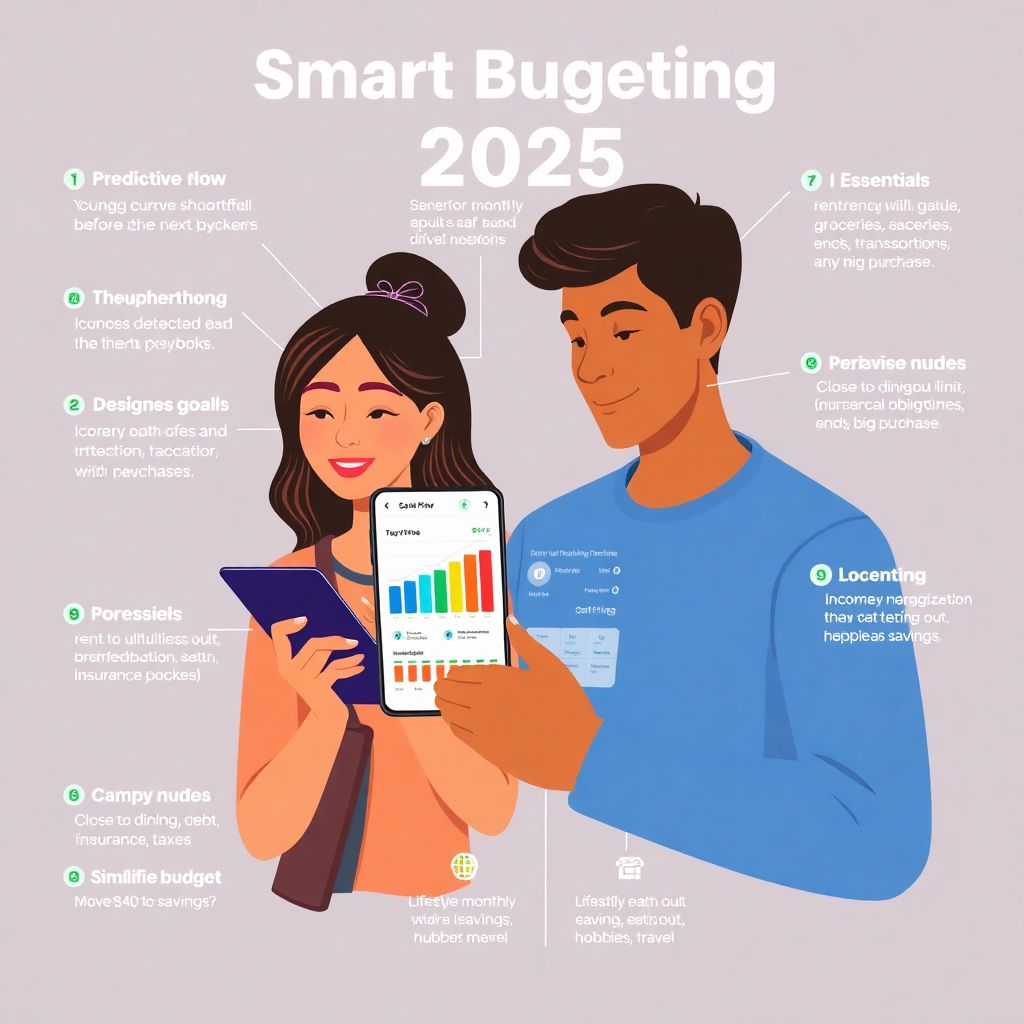

Smart tools aren’t just pretty dashboards. They actively help you make decisions. Typical features of smart budgeting tools for managing money include:

– Predictive cash flow: the app warns you if your current pace of spending will leave you short before the next paycheck.

– Subscription detection: it highlights recurring charges and unused services.

– Goal tracking: it shows how every extra $20 you set aside affects the date you’ll fully fund your emergency fund or vacation.

– Behavior nudges: small, timely suggestions like “You’re close to your dining-out limit for this week.”

By 2024, the global personal finance software market was estimated at around $1.5–2 billion, and analysts project annual growth in the 12–15% range through 2030. The main driver is that banks and fintechs are racing to integrate these tools directly into their apps. For beginners, that means budgeting will increasingly show up “by default” inside your bank, rather than as a separate app you have to discover.

Economic context: why your budget matters more than ever

Inflation, real wages and household stress

Over the past few years, many countries experienced elevated inflation, and while headline rates are easing in 2025, prices remain structurally higher than before 2020. In parallel, real wage growth for middle-income households has been modest. That gap between how fast costs rose and how slowly income caught up is one of the reasons so many people feel they are always behind.

Macroeconomists point out that when large portions of the population adjust spending in response to higher uncertainty — for example, cutting discretionary purchases, postponing big-ticket items — it affects entire sectors: retail, hospitality, travel, personal services. Individual budgeting behavior scales up into macroeconomic patterns.

Smart budgeting, oddly enough, can stabilize things a bit. When households build even small emergency funds and gain predictable cash flow, they are less likely to panic-cut all non-essential spending in a downturn. That cushions shocks for local businesses and helps smooth consumer demand.

Debt, credit scores and long-term costs

Another economic aspect: interest. In many countries, credit card APRs and consumer loans are still high. If you don’t track your balance and spending, you’re effectively giving away future income to interest charges.

Here smart budgeting tools make a measurable difference. Apps that show you, in real time, how much interest you’ll pay across different debts if you pay only the minimum versus a bit extra can change behavior. Studies from 2022–2024 show that when people see visual projections of their debt payoff timelines, they are significantly more likely to increase payments — even by small amounts that add up over years.

From a system-wide view, better household budgeting supports healthier credit portfolios for banks, fewer defaults and more stable lending conditions. The micro and the macro are tightly linked.

Simple tactics that work in real life

Fast, low-friction wins

People often ask for simple budgeting tips to save money fast because they’re under pressure: an upcoming bill, a debt payment, or just the desire to stop feeling broke by day 20 of the month. While there’s no magic trick, there are several low-friction moves that consistently help beginners:

– Name your money before you get it. Decide on paper or in an app what every paycheck will do (bills, savings, fun) before it lands.

– Cap lifestyle categories weekly, not monthly. It’s easier to avoid overspending on restaurants if you see a weekly cap than trying to remember at the end of the month.

– Attack subscriptions once per quarter. Spend 20 minutes every three months canceling or downgrading — this alone can free up 5–10% of your monthly outgoings.

These steps don’t require you to become a finance nerd. They simply reduce autopilot spending.

Behavioral science: why we overspend

Overspending isn’t only “lack of discipline”; it’s also design. Apps, checkout flows and marketing are optimized to reduce friction when you spend, not when you save. One-click purchases, personalized offers and buy-now-pay-later services are all based on decades of behavioral research.

Smart budgeting tools are the counterweight. They reintroduce small, strategic frictions: alerts when you exceed a category, “are you sure?” prompts when a purchase threatens your goals, or a simple progress bar that you don’t want to reset to zero. In experiments by fintech companies, adding a single pre-purchase “goal reminder” screen reduced impulse spending by meaningful margins, especially for younger users.

Impact on the financial industry

From isolated apps to embedded finance

For banks and fintechs, beginner-friendly budgeting is no longer a “nice extra”; it’s a competitive feature. Over the last few years, traditional banks have seen that users who actively use budgeting and goal tools are more loyal, maintain higher average balances and are less likely to churn.

As a result, we’re seeing three major shifts:

– Embedded budgeting: banking apps now include automatic categorization, cash-flow projections and savings “vaults” by default.

– Partnerships with budgeting startups: many incumbents prefer integrating existing best-in-class tools rather than building from scratch.

– Data-driven personalization: anonymized spending data powers more accurate financial advice and product recommendations.

This industry response creates a kind of positive feedback loop. As tools become more seamless and visible, more beginners try them; as usage grows, providers invest further in smarter features.

Data, privacy and regulation

There is a flip side. Smart budgeting relies on detailed transaction data, and sometimes even geolocation and behavioral signals. That raises privacy and regulatory questions. Open banking rules in regions like the EU and UK already require strict consent and security protocols; similar frameworks are expanding in other markets.

By 2025, regulators are increasingly focusing not just on data protection, but also on “algorithmic fairness” — making sure automated advice doesn’t systematically disadvantage certain groups. For users, this likely means clearer disclosures, standardized data-sharing permissions and, in the longer term, easier portability of your budgeting history between apps.

Looking ahead: the future of smart budgeting

Forecasts for the next 5–10 years

Analysts expect the smart budgeting ecosystem to evolve along three main axes by 2030:

1. Hyper-personalization. AI models will learn your unique patterns — pay cycles, cultural holidays, irregular income, even your tendency to splurge under stress — and offer ultra-specific advice: “Shift this bill by three days” or “Move $40 from fun to transport this week to avoid going negative.”

2. Automation of boring decisions. More people will let tools automatically move “surplus” money to savings, adjust goal contributions when income changes and even renegotiate certain bills. The budget becomes a living agent, not just a static plan.

3. Integration with life events. Expect budgeting modules directly inside tax software, HR portals, education platforms and even health apps, linking financial decisions with career moves, study plans or medical costs.

Market research firms project that user penetration of personal finance and budgeting apps could approach 40–50% of adult smartphone owners in advanced economies by 2030, up from roughly 20–25% in the early 2020s. Among Gen Z and younger millennials, adoption rates are likely to be significantly higher, since these age groups already treat their phones as financial “command centers”.

Will budgeting become invisible?

Paradoxically, the more advanced tools become, the less you’ll think about them. Smart fridges that track groceries and update food budgets, cars that integrate fuel costs into your monthly plan, subscription hubs that auto-suggest cheaper bundles — much of what we now call “budgeting” will run in the background.

But one element won’t disappear: values. No app can decide what matters to you: travel vs. home ownership, work-life balance vs. rapid career growth, family support vs. personal projects. The real role of smart budgeting in 2025 and beyond is to clear the noise so you can connect daily spending to those bigger choices with less stress and more clarity.

To wrap up, starting as a beginner in this landscape doesn’t require perfection. It requires one deliberate step: picking a simple method and one or two tools you’ll actually use. From there, the technology, economic context and industry innovations are increasingly on your side — turning what used to be a chore into a practical, data-informed habit that quietly compounds in your favor year after year.