Essential Tools to Kickstart Your Budgeting Journey

Before diving into the numbers, it’s important to set yourself up with the right tools. As a beginner, you don’t need anything fancy — just something that helps you stay organized and consistent. Many people get overwhelmed by complex spreadsheets or financial apps with too many features. Start simple and grow from there.

You can choose one of the following:

– Pen and paper: Yes, the old-school method still works. A notebook dedicated to your finances can be surprisingly effective.

– Spreadsheets: Google Sheets or Excel are great for tracking income and expenses if you’re comfortable with basic formulas.

– Budgeting apps: Apps like Mint, YNAB (You Need a Budget), or EveryDollar are beginner-friendly and offer helpful visuals and reminders.

Whichever tool you pick, the key is consistency. If you prefer writing things down, don’t force yourself into using an app. The best tool is the one you’re actually going to use.

Step-by-Step Guide to Building a Realistic Budget

Step 1: Track Your Income

Start by figuring out exactly how much money you bring in each month. Include your main salary, freelance gigs, side hustles, and any passive income. Don’t guess — check your bank statements or pay stubs. If your income varies, take an average of the past 3-6 months to get a more stable figure.

This is your foundation. You can’t build a realistic budget if you overestimate how much money you have coming in. It’s better to be conservative here — plan for the lower end of your income range.

Step 2: List All Expenses

Now it’s time to get real about spending. Go through your last 1-2 months of bank and credit card statements. Separate your expenses into fixed and variable costs:

– Fixed expenses: Rent, mortgage, car payments, insurance, subscriptions.

– Variable expenses: Groceries, gas, dining out, entertainment, shopping.

Don’t forget irregular expenses like annual insurance premiums or holiday gifts. A good trick is to divide those by 12 and include a monthly portion in your budget.

Step 3: Categorize and Prioritize

Once you’ve listed your expenses, group them into categories that make sense to you. For example: housing, transportation, food, health, personal, savings, and debt payments. Assign a realistic dollar amount to each category based on your past spending — then look for areas you can adjust.

Ask yourself:

– Am I spending too much on takeout?

– Can I cancel unused subscriptions?

– Is there room to increase my savings?

Step 4: Set Financial Goals

Budgeting isn’t just about tracking money — it’s about giving every dollar a purpose. Define short-term and long-term goals that motivate you. Maybe you want to build a $1,000 emergency fund, pay off credit card debt, or save for a vacation.

Once you’ve set your goals:

– Allocate a portion of your income toward them each month.

– Track your progress and celebrate milestones.

Having goals makes it easier to say no to impulse purchases because you’re working toward something bigger.

Troubleshooting Common Budgeting Problems

Problem: Going Over Budget Every Month

Spending more than you planned? You’re not alone. This usually means your budget isn’t aligned with reality. Go back and check your spending categories. Did you underestimate how much you spend on groceries or gas?

Try these tips:

– Use cash envelopes for problem areas like dining out or entertainment.

– Set spending limits and use mobile alerts to track progress.

– Plan for small indulgences so you don’t feel deprived.

Problem: Irregular Income Makes It Hard to Plan

If your income changes month to month, budgeting can feel impossible. But it’s doable with a little buffer planning. Use a “baseline budget” — the minimum income you expect — and base your essentials on that. Any extra income can go toward savings, debt, or non-essentials.

Keep a list of priority expenses in case you need to cut back. Flexibility is your superpower here.

Problem: You’re Losing Motivation

Budgeting fatigue is real. After a few months, you might feel like giving up — especially if you’re not seeing immediate results. To stay motivated:

– Review your goals regularly and adjust them if needed.

– Celebrate small wins, like paying off a credit card or saving $100.

– Involve your partner or a friend for accountability.

Remember, budgeting is a skill — not a one-time task. You’ll get better with time, and the results will follow.

Expert Tips to Make Your Budget Stick

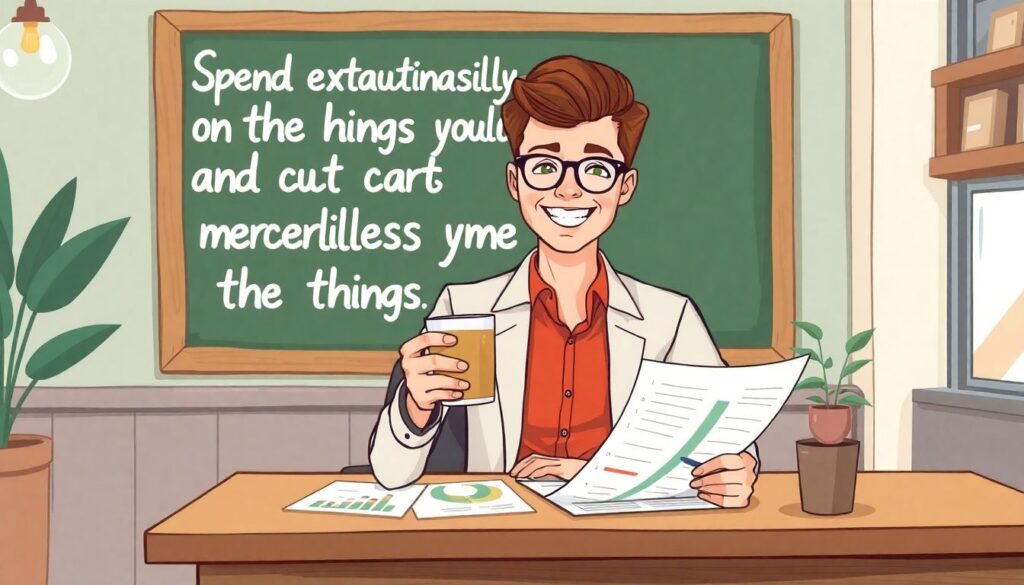

Financial experts agree on one thing: your budget should reflect your real life, not a fantasy. According to certified financial planner Ramit Sethi, “Spend extravagantly on the things you love, and cut costs mercilessly on the things you don’t.” That means if you love coffee shop lattes, keep them — just find savings elsewhere.

Other expert-backed tips:

– Automate savings and bill payments to avoid forgetting or overspending.

– Review your budget monthly and adjust as your life evolves.

– Keep it flexible — a rigid budget is more likely to break.

Creating a realistic home budget isn’t about restricting your life. It’s about giving your money direction so you can live with less stress and more freedom. Start simple, stay consistent, and don’t be afraid to make changes as you go.