Historical Background

The Origins of Financial Independence

The concept of financial independence (FI) is not novel. Its roots trace back to early 20th-century ideas about frugality and self-sufficiency, most notably championed during the Great Depression. People learned to live within tight means, not out of choice but necessity. However, the modern FI movement truly began to take shape in the 1990s with the publication of *Your Money or Your Life* by Vicki Robin and Joe Dominguez. This influential book introduced the idea that money represents life energy, and that personal finance should be aligned with values, not just consumption. The FIRE movement (Financial Independence, Retire Early), which gained momentum in the 2010s, brought these ideas mainstream. Today, FI is no longer a fringe philosophy — it’s a practical lifestyle choice for those seeking autonomy and purpose.

The Shift in Mindset Over Time

In recent decades, the narrative around money has shifted. While older generations viewed retirement as something achieved at 65 through a pension, millennials and Gen Z are redefining success. With unstable job markets, rising living costs, and a digital economy, younger generations have embraced minimalism, remote work, and passive income strategies. Financial independence has become a form of resistance to consumer culture — a path that prioritizes time and freedom over material accumulation.

Core Principles

Spend Less Than You Earn

At the heart of financial independence lies a simple truth: you must consistently spend less than you earn. This margin allows you to save and invest, thereby building a financial cushion. Experts like Mr. Money Mustache, a prominent voice in the FI community, advocate for aggressive savings rates — sometimes as high as 50–70% of income. While this may seem extreme, even a modest 20–30% savings rate can drastically reduce the time it takes to reach independence.

Invest Early and Often

Compound interest is a powerful ally. Starting early, even with small amounts, gives your investments time to grow exponentially. The general advice from financial planners is to invest in low-cost index funds, which offer diversification and low fees. As noted by certified financial planner Sophia Bera, “You don’t need to beat the market to win. You just need to be in the market long enough.” Automating your investments is a critical move — it removes emotion and ensures consistency.

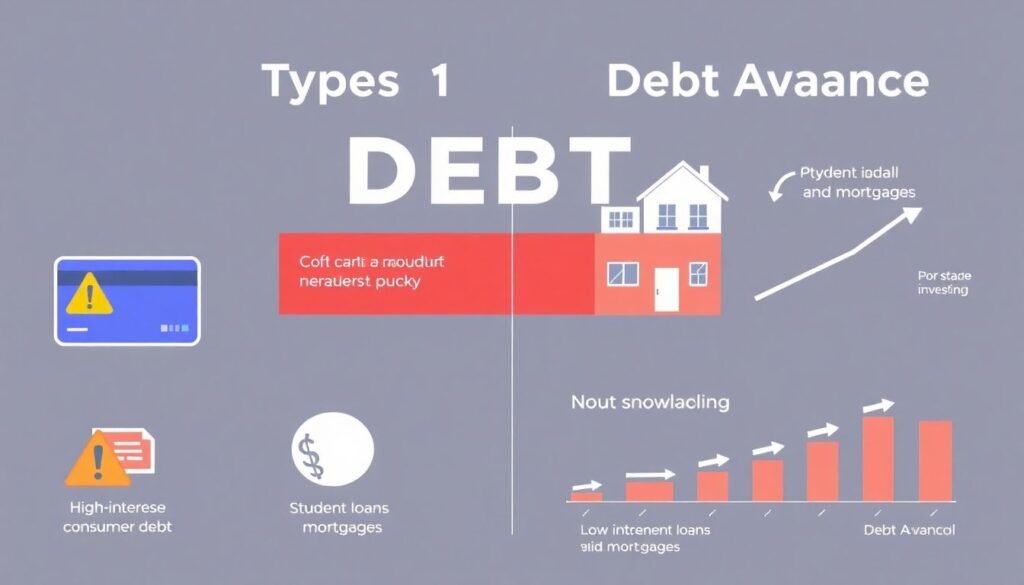

Eliminate Debt Strategically

Not all debt is created equal. While high-interest consumer debt (like credit cards) should be paid off immediately, low-interest student loans or mortgages can be managed alongside investing. The debt snowball and debt avalanche methods are popular among FI enthusiasts. The key is to avoid lifestyle inflation — as your income grows, resist the urge to increase spending proportionally.

Define Your “Enough”

Financial independence isn’t about being rich — it’s about having “enough.” This requires a deep understanding of your values and goals. Establish what kind of life you want to live and calculate the amount of money needed to sustain it. This is often referred to as your FI number — typically 25 times your annual expenses. Knowing this target gives clarity and purpose to your financial actions.

Real-Life Examples

The Frugal Engineer

Take the case of Liz Thames, also known as the Frugalwoods. She and her husband reached financial independence in their early 30s by living on a fraction of their income and investing the rest. They left high-paying jobs in the city to live on a homestead in rural Vermont. Their story illustrates that FI is not about deprivation — it’s about intentional choices.

Urban Minimalist Lifestyle

Consider Jamal, a software engineer in Chicago, who adopted a minimalist lifestyle after reading about FI. He sold his car, moved into a smaller apartment, and started biking to work. By cutting expenses and investing aggressively, he achieved financial independence by age 38. His story shows that urban living and FI are not mutually exclusive.

Digital Nomad Path

Emma, a freelance writer, combined location independence with financial autonomy. She moved to lower-cost countries, reduced her living expenses, and used geo-arbitrage to save more. By building multiple income streams online, she reached a point where work became optional. Her case demonstrates how digital tools can accelerate the road to financial freedom.

Common Misconceptions

“You Have to Be Rich to Start”

One of the most persistent myths is that financial independence is only possible for high earners. In reality, the journey is more about discipline than income. Many people with average salaries have achieved FI through consistent saving and smart investing. It’s not how much you earn — it’s how much you keep.

“FI Means Quitting Your Job”

Another misunderstanding is that reaching FI means you must retire early and never work again. In truth, many people continue working after achieving FI — but on their own terms. They pursue passion projects, part-time gigs, or entrepreneurial ventures. The point is not to stop working but to remove the obligation to work.

“It’s Too Late to Start”

Some believe that if they haven’t started by their 20s, it’s too late. This is false. While earlier is better due to compounding, many people begin in their 40s or 50s and still achieve significant financial autonomy. The key is to start now, with what you have, and build momentum.

Expert Recommendations

Start With a Detailed Budget

According to financial coach Ramit Sethi, “You can’t optimize what you don’t track.” Begin by creating a zero-based budget — assign every dollar a purpose. Use tools like YNAB (You Need a Budget) or spreadsheets to monitor progress. This clarity is essential for identifying leaks and opportunities.

Automate Your Finances

Set up automatic transfers to savings and investment accounts. This removes temptation and ensures you pay yourself first. As noted by personal finance expert Paula Pant, “You can afford anything, but not everything.” Automation helps prioritize what matters most.

Build an Emergency Fund

Before investing aggressively, secure a safety net. Most experts recommend 3–6 months of living expenses in a high-yield savings account. This buffer prevents you from dipping into investments during emergencies, preserving your long-term strategy.

Surround Yourself With Like-Minded People

Environment shapes behavior. Join online FI communities, attend meetups, or follow blogs and podcasts in the FIRE space. Learning from others not only educates but also reinforces your commitment. As financial advisor Carl Jensen puts it, “The journey to financial freedom is easier when you’re not walking alone.”

—

Financial independence is not a fantasy reserved for the wealthy or the ultra-disciplined. It is a practical, achievable goal rooted in intentional living, strategic planning, and long-term thinking. By embracing its principles and learning from those who’ve walked the path, anyone can transition from budgeting to freedom — one smart decision at a time.